by Jenny Smedra

I spend my entire work week online, reading and writing about personal finance. Lately, I have been browsing through tons of sites, discussion boards, and forums designed for people dealing with debt and bad spending habits. However, a post from a woman in Alaska highlighted a problem we all face. In her original post, the woman detailed her family’s current debt, seeking advice and support. Before I delved into the comments, I found myself wondering how this could happen. Furthermore, how many other people found themselves in similar circumstances?

Identifying the Bad Spending Habits That Got You Here

Car and Vehicle Loans

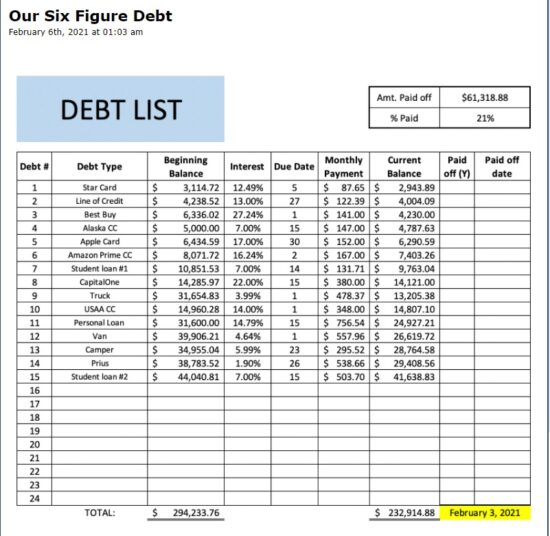

At first glance, I was blown away by how much money they owed for car and vehicle loans. When totaling the remaining balances on their truck, van, camper, and Prius, it amounted to approximately $98,000. That is just about half their debt! However, I knew there had to be more to the story. So, I combed through the comments to understand why a couple so deep in debt would take on the burden of so many vehicles.

Buying Second-Hand to Avoid Costly Car Payments

While most of the vehicles were necessities, there were some great points from other commenters about the newest one. The family bought the Prius for their side job delivering DoorDash. While it is commendable to find ways to bring in more money, buying a new car for it seems counterproductive. It would be much more economical to purchase a used car instead of taking on an additional monthly car payment.

I feel like many of us fall victim to this consumer mentality. We feel the need to have the latest or newest things, myself included. Although I have always wanted a new car, I had to be realistic and buy vehicles that fit my budget. Anytime I was tempted to look at new vehicles, my dad also reminded me they lost value as soon as you drove them off the lot.

Furthermore, if you can’t meet the monthly payments, the dealership turns your loan over to a debt collection agency. In the worst case scenario, you could have the vehicle repossessed, leaving you stranded and still in debt. Even if you do a voluntary repossession, you may still find yourself paying for a vehicle you don’t even own.

Credit Card Debt

The next piece of the puzzle that stood out was the overwhelming balances on their credit cards. Having dealt with five-figure credit card debt, I understand how easily credit card balances can slip beyond your control. The convenience of shopping online makes it even harder to break bad spending habits. It becomes difficult to resist temptation, especially when you feel like there is no way out. If I was already that deep in debt, what was a little more going to hurt? However, my loved ones reminded me that there is always hope. That’s when I contacted debt relief program for a free consultation to help me get back on track.

Tackling Credit Card Debt

The first step in tackling credit card debt is to determine where you’re spending your money. Once I identified my bad spending habits (travel and transportation), I cut up those credit cards and transitioned to a bare-bones budget. It was an uncomfortable adjustment, to say the least. I sacrificed many creature comforts and indulgences for the cause. But, I knew that if I wanted to climb out of my financial hole, I had to stop digging. In the end, I was able to clear my credit card debt in less than two years. Thanks to strict self-discipline and a limited budget, I was finally debt-free.

The Debt Avalanche Method

Now, we can’t be certain what constitutes this family’s credit card debt. However, the outstanding balances with Best Buy and Apple suggest that electronics are the main culprits. While technology is expensive, the worst part about store credit cards is that that also come with much higher interest rates. Their Best Buy card has a whopping rate of 27.24%!

If you are strapped with several high-interest debts like these, the debt avalanche method probably makes the most sense for you. In contrast to the debt snowball, the debt avalanche method targets your debts with the highest interest rates first. After making all your minimum payments, any leftover funds should go to balances on these cards. Paying off these debts first will save you more in interest and lower your monthly payments over time.

How Bad Spending Habits Affect Those Around You

Including Your Partner

Reading through the comment section, one pattern was very clear. The OP openly shared her struggles to get her husband on the same page. She explained how difficult it was to get him to stop using the credit cards and spending money they don’t have. Speaking from personal experience, this resistance creates tension in both your finances and personal relationship. If you and your partner are not working towards the same goal, then you are already fighting a losing battle. If you want to make any progress in paying down your debt, then you need to make sure your priorities align.

Setting an Example for the Next Generation

One of my greatest concerns is about the example I am setting for the next generation. Although I am no financial expert, I know that children watch and learn from their parents’ spending habits. How we handle money forms their attitudes, behaviors, and beliefs about their own finances. If we are unable to identify and correct our own bad spending habits, it increases the chances that our children will also face the same challenges. That was enough motivation for me to break the cycle.

Even if you have good intentions, you have to make a budget and start implementing it. It is a long arduous journey, but you have to begin somewhere. Even when faced with six figures of debt, there is hope. You can start budgeting as a family, and include children in some of the discussions. While they don’t need to know all the details, we can all use support to stay on track to reach our financial goals.

Read More

- Stuck in Student Loan Debt: How I Paid Off $81,000

- Finding Medical Debt Forgiveness: 5 Ways of Getting Out of Medical Debt

- 6 Best Repayment Strategies for Paying off Debt Once and for All

Jenny Smedra is an avid world traveler, ESL teacher, former archaeologist, and freelance writer. Choosing a life abroad had strengthened her commitment to finding ways to bring people together across language and cultural barriers. While most of her time is dedicated to either working with children, she also enjoys good friends, good food, and new adventures.

This is a weird post. How did you come across an obscure, brand new blog? Is this someone you know, or another blog owned by the owners of BAD? If not, this is a mean spirited post, like you are just posting to point to someone with bad spending habits

This feels like a really bad joke – who in their right mind would buy a camper to live in (then not live in, but continue to keep) and also a Prius to DoorDash?

For goodness sake – sell the Prius and Camper and put that money immediately to your high interest credit cards!

And stop digging a hole!!!

Wow!!! I hope they can work on this debt or they already have. I am luckily able to afford cars because of generosity and saving – and I would never take a payment plan, unless I made wayyyyy more money. Even then, I would just save up until I could afford another car.