by Ashley

Looking back at some old posts I see that I’ve had some lofty financial goals. It reminds me of this saying:

“Shoot for the moon. Even if you miss, you’ll land among the stars.”

(Google says the quote is by Normal Vincent Peale)

Well, I guess I’ll have to settle for the stars, because I’ve missed my moon. But that’s okay. Progress is still progress. I just wanted to look back and remind myself of where I’ve been and where I’m going….

In this post I had listed my goals in terms of debt repayment. You’ll notice that my goal date to be rid of our license fees was originally August 2014. August came and went, and we still have those monthly license payments.

In this later post I changed my mind and decided to put my Race to 20K (paying off the car loan) above everything else. At the time I was hoping to pay $3,000/month toward the car loan. Yeah….that hasn’t happened either (aside for I think one or two months??)

And recently I’ve hinted at maybe changing my plan of action again. Re-ordering my debt payoff journey. You guys are right. The APR on some of my student loans is outrageous. Why not knock it out and then turn my attention to the car? In the past few months when I haven’t been able to pay $4,000 or $5,000 toward debt it changes the whole payoff schedule. Why not earn some “easy” wins by knocking out some of the smaller debts instead of tackling the comparatively huge car loan that could takes months to pay off?

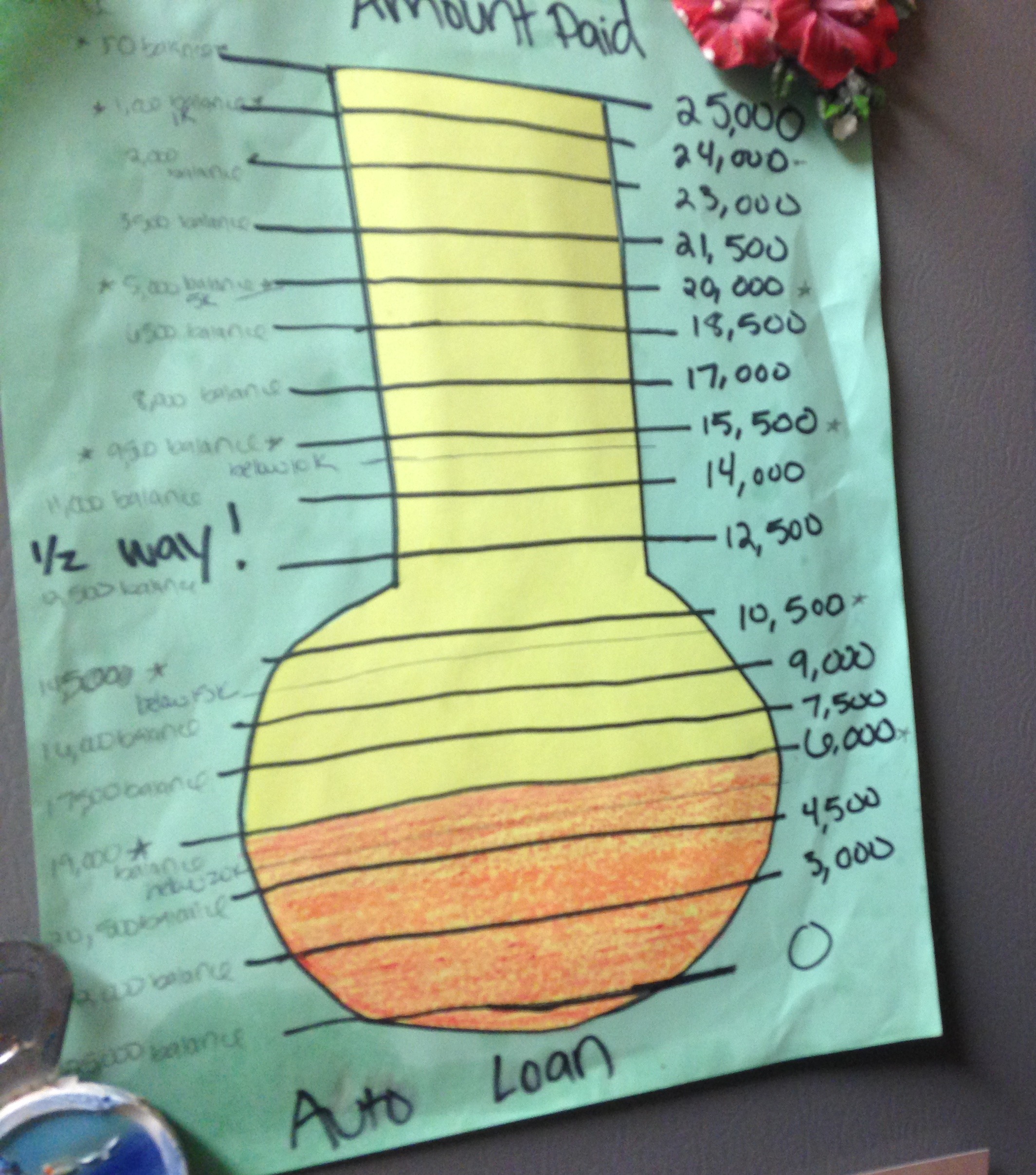

And then I walk into my kitchen and see my auto loan debt thermometer. And I am absolutely re-energized.

I guess that’s the thing about personal finance. It’s personal.

No, it doesn’t make sense. Any financial guru you talk to will say I’m doing it wrong. Either you’ll hear from the Ramsey types who say my car loan is too big and I need to start by tackling a smaller loan. Or you’ll talk to a numbers person who will say the APR on my car loan is peanuts in comparison to the student loan APRs, so I should start with the highest APR. No one would say that tackling the car first is the “right” thing to do. Or would they?

Whatever is the most motivating might make the most sense, too. Right?

I mean, I want all of my debt gone. I’m so, so, so sick of it! Having the little financial set-backs this month (with the car repair and house flood) have just reaffirmed how much I hate this debt. It’s so burdensome! It’s like a noose around the neck that we just can’t get rid of! Getting rid of the debt, in so many ways, will feel like earning our freedom back!

But so much of the journey is psychological in nature. And even as I’m doubting myself and thinking, “maybe we should just kill that high interest student loan real quick”….I just keep coming back to my starting place. And I see our car. And I want it to be ours for real.

I know it’s not the popular decision. With all my recent payments and hard work recently we are no longer upside down on the loan, either. I know many would say we need to sell it and rid ourselves of the nearly 20 grand (now actually right at 18 grand) of debt in the snap of our fingers. But it’s just not that easy.

We love our car (actually an SUV, a 2011 Ford Explorer). With the long road-trips we take we need something large enough to accommodate two car seats, a double stroller, us, our dog, our luggage, and cooler of food/drinks/snacks. That’s really not do-able in a car or even a cross-over. A van could work, but it doesn’t feel right to make that type of trade. The way I see it, we’d be able to sell our SUV for $20k, buy a reasonable used van for $10k, which leaves us with $10k less debt (and a paid for van). But as soon as we’re done paying off other debts we’ll go right back to selling the van (plus putting in extra $$) in favor of finding another SUV. Why? Why not just pay it off and own it outright from the start and save ourselves the headache of all the buying and selling and trading of vehicles?

I didn’t want to have to put it all out there like this because it sounds like nothing but excuses and rationalizations. I know it will anger some of you. But we’ll just have to file this under the “agree to disagree” label and call it the “personal” part of personal finance.

So there you go. The plan remains.

But don’t be surprised if I end up wanting to come back to re-visit this again at some point in the future. It never hurts to reassess one’s goals, particularly in light of big income changes. Hopefully with all my applications we’ll be having another big income change sometime soon….only this time going upward! : )

What debt are you currently working on paying off? What method of debt repayment do you follow (smallest to largest? Highest APR first? Psychological satisfaction?)

Hi, I’m Ashley! Arizonan on paper, Texan at heart. Lover of running, blogging, and all things cheeeeese. Early 40s, married mother of twins, and working in academia. Currently working toward financial independence with the goal of (hopefully!) retiring early at 50.

You are right: Personal Finance is Personal.

If I were in your shoes, I probably wouldn’t get rid of the car too, but I would tackle the high interest rate debt first. Interest is such a waste.

Take care…

I prefer paying off the smallest balances, regardless of interest rates. I need the see the success of paying something off to keep me motivated. I also like being able to put the money I was paying toward one bill on another balance. It’s discouraging to me not to feel the progress of paying something completely off. You’re right, it’s personal. The end goal is to get the debt paid off. If you don’t reach the end goal because you get discouraged by your system, the small savings in interest that would have been achieved by following a different system is meaningless.

I’d stay with the SUV. I have a 2005 Ford escape that we love. We don’t owe as much not it, but this vehicle fits us perfectly. We’ve had cars in the past and they were fine. I feel safer in the SUV and we live on a back road which is especially bad in the winter–gotta love my 4 wheel drive. You couldn’t pay me to enough to get a mini van. I can’t stand them would much rather have an SUV. It’s your choice and you stick with what suits you. I know a lot of people always go for small cars due to gas mileage. I personally want a 6 cylinder vehicle and am willing to pay more for gas. We live in the country with tons of big hills–I need power especially in winter! Plus don’t want a small car in case I’m in an accident with a deer or moose. Needless to say you don’t see many smart cars up here. Man you hit a deer or anything in one of those and you would be dead.

Yikes! Yes, that would truly be dangerous! Even for regular city-driving….can a smart car even survive an accident or would it simply be totaled? Not to mention the person inside it – seems scary!

When I first got serious about debt repayment I tackled my car first, so I understand Ashley’s reasoning. I’m working on the student loans now. So far this year I paid $12,000 towards it. You have been doing a great job Ashley, keep at it!

That’s awesome Juju!!! Keep up the good work!!!

I think you have to do what keeps you motivated. I can’t say I agree with the car decision however when you are on a path for the long haul, you have to do what keeps you psyched. And if that’s keeping the SUV, then do that:)

On a unrelated (sort of) side note, I did something last night that was really helpful to me. I decided to go through my emergency expenses for last year and this year, to get an idea of how much “my” emergencies (Murphy’s) were costing me….in 2013, they were roughly $3870 and in 2014, it was $2490. That little exercise helped me understand just how much cash needs to be really liquid. I have a dental emergency so I’ll need to set up an appointment later today which will add to my emergencies for 2014. That’s what prompted me to think about my emergency fund, lol. Anyway, I know you have a lot on your plate but this little exercise of adding up my emergency expenses was really enlightening. I tended to vastly underestimate my emergency needs. Before this little exercise, I thought it was around $1000-$1500 per year. Now I know that I need to keep $3-4K readily available on top of everything else so I won’t be caught off guard.

That’s a really good idea! I’m planning to go back and take a close look at this full year sometime in January so I can really try to get an accurate assessment of things. Makes sense to look at emergencies (and Murphy’s law stuff) when I do that, too!

I hope you don’t get hung up on the keep/don’t keep the car because you really have made up your mind. Instead have you looked at how much you are paying a year in interest on those student loans? If you make your minimum payment on the car loan and then pour all the rest into the higher interest loans your debt will drop faster. Add to that the fact that the student loans are unsecured so you can’t sell the item to pay them off and they can’t be eliminated by bankruptcy and you will have them around your neck for a long time if you don’t prioritize them. Why not just make a new thermometer for your frig with the student loans on it and get motivated to see your payoff there?

I could certainly do a debt thermometer for the loans too, but it doesn’t feel the same. It’s hard to explain because, yes, I want ALL my debt gone. But the student loans don’t get me riled up the same way my credit cards did (or the same way my car loan currently does). The high APR certainly gets me riled up, but I don’t think I’d feel the same satisfaction from knocking out the student loans as I would the car. I don’t know. Like I said, I may re-visit this again in the future too so I don’t want to say this is an absolute statement and I will never consider it again. But for right now I still really want to focus on the car.

I kinda think along the same lines as Juhli. You want to keep the car and that makes sense to you so not arguing there.

My thinking is not only are the interest rates on those loans high, the balance is also comparatively small. Why not just knock it out in a month or 2. and then get right back to get rid of the car like you want. Map it out, the car might actually be paid off faster with that snowball added in. just my 2 cents.

Ehhhh, this would take a little time and a little math so maybe I can do this sometime the coming week. But, remember, in total I have over 100K in student loan debt. There is absolutely no way it will be paid off before the car is paid off. Yes, I could pay off a couple of the higher interest student loans (I’ve got an 8.5% and an 8.25% both at about a 5,000 balance), and I could knock those out but, again, they just don’t give me the same intrinsic motivation that the car loan gives me. I’ll have to think about it a little further.