by Hope

Ran an ad campaign for a “on the fence” client recent or rather, still.

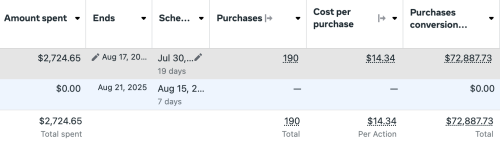

I created the assets (graphics), copy, and determined the strategy. And I ran it. Starting with a $250/day budget. (Client pays add spend.)

To date, I’ve made them just over $72K with an ad spend of $2.7K. For a ROAS of nearly $27 for every $1 spent. Not too shabby.

To be honest, it is an easy product to sell, and I know this audience. Very well. So the psychology of the messaging and finding the right audience was easier than most of the campaigns I am charged with.

Today I received a phone call from the CEO of the company. He gave me a bonus – paid out as soon as our phone call was over. And has verbally agreed to an extension of my contract. Or rather a new contract with new deliverables.

It’s been a few years since I received a Bonus for my work. As far as I know, it’s not a common thing in the contractor world.

The Plan

So what am I going to do with it? I knew you would ask. (It’s $1,000 so I should end up with $600-700.)

Outside of taxes, gov fees, the entirety will go to savings. My dad and I have been talking. He’s kind of my accountability partner. And certainly who I bounce my ideas off of. It’s nice to have one of those after decades of doing things alone.

He would like me to get to $10K in my Ally savings account, $1K in my EF (easily accessible account, and then focus solely on paying off my remaining debt.

What do you all think of this plan?

If all goes well this month, I think I might hit those savings goals. Then turn my attention to my debt alone (outside of the auto-transfers to savings and investments totalling $125 per week.)

Thoughts?

Hope is a resourceful, solutions-driven online business manager with over two decades of experience helping clients streamline operations, manage projects, and grow their businesses through digital marketing and technology.

But life has a way of rewriting your plans.

A year ago, Hope made the decision to move in with her aging parents full time – a season she wouldn’t trade, even as it came with its own financial and emotional weight. Earlier this year, she lost her mother, and is now walking the tender, disorienting path of grief while learning what “forward” looks like from here.

Hope came to the Blogging Away Debt community in 2015 as a single mom raising five foster and adoptive children. She’s written through job changes, financial setbacks, and the bittersweet transition to an empty nest. Her kids are finding their footing in the world now – and so is she.

Rooted in faith and fueled by the same perseverance she’s brought to every hard season, Hope is ready to face her finances with fresh eyes and an honest pen. She believes that clarity, courage, and community can change the trajectory of anyone’s story including her own.

She lives in Austin, TX with her dad, loves adventures with her dog Addie, and is figuring out, one step at a time, what this next chapter is meant to be.

100% on board with the 10k in ally.

Iffy on the debt repayment….you finally paid off all your debts except that pesky student loan (I’m assuming this is still correct? – get rid of anything new)…that student loan interest rate of 2.875% is SOOOO low. I’d honestly keep it for life. (is that 2.875% permanent? if not, get rid of it).

My 2 cents (worth nothing): get to the 10k in ally, then focus on your retirement. at the very least max out an IRA (traditional for the tax breaks), but ideally max out an i401k.

Honestly, I’d start knocking out those student loans. Dave Ramsey would say to. They don’t seem to have budged much in years. Its really not that much, but in your 50s I wouldn’t want to be paying student loans every month. Knock it out.

I have mixed feelings. She is making $307 payments and based on her interest I would expect these to be paid off before she would be eligible for retirement( around sixish years) The bad part is Hope has a bad habit of these going into deferments when stuff goes sideways and she is going to be cutting it close into retirement when I definitely would not my Social Security or savings going towards this payment rather than my everyday needs. Hope do you qualify for Social Security at this point and have any idea what you will collect? This is where a budget comes into play. In your 50s you should be paying debt down to minimize what your expenses will be so that in your 60s you are set to go if you need to live on a fixed income for the rest of your time here. You have ALOT of uncertainty with no idea on what you will need to pay for housing. I live in a somewhat inexpensive part of the country and houses go for at least $200,000 here. While it would not be impossible to cash flow that amount I find it hard to think you could cash flow it while simultaneously saving some to supplement social security. If I were Hope I might take some of my allowance and apply it towards this debt to pay it off earlier an extra hundred would be an extra $1000 a year to get it done earlier. It’s really hard to help her when you don’t have a complete picture.

My feelings about your remaining student loan:

Going purely by interest rate analysis, you should pay the student loan only if you are reasonably sure you won’t incur consumer debt anymore. At 3%, let alone equities over 10 years. So right now, that loan is like free money from an investment returns perspective.

If you want to approach this with the Dave Ramsey philosophy, yes you would pay this loan but only after making a complete, zero-based budget fulfilling the following:

1. demonstrates realistic commitment to no new debt ever again

2. maximizes available cash for speedy and intentional repayment

You are not consistently conforming to those budgetary requirements as of yet. Dave Ramsey doesn’t take on the 2 numerical arguments I give above because he argues his method works psychologically and emotionally to convert people away from a debt-happy lifestyle. So, I’m saying if you want to toe his line on paying all debt regardless the numbers, you should to do the whole budget his way. And if you do go DR, do the budget and debt stuff only and not his investment advice.

One other argument for paying this SL is to eliminate the monthly payment obligation. However, you only see this benefit once the loan is paid off. I’m not sure at that low interest rate this is worth the risks of the 2 numerical arguments I give above.

My comment got truncated after submission, I think due to interpreting less than and greater than symbols as html tags (yikes at not cleaning website input!!). These are the intended top 2 paragraphs:

Going purely by interest rate analysis, you should pay the student loan only if you are reasonably sure you won’t incur consumer debt anymore. At less than 3%, you will lose a lot to interest if you pay down SL then later end up carrying a cc balance or take a personal loan.

The other numerical argument against paying this student loan is that you still have 10+ years to retirement age, so you will almost certainly see better investment returns from an appropriate investment portfolio aimed at your retirement age. Paying this loan is a guaranteed 2.875% return and as of today money market and high-yield savings accounts yield more than 3%, let alone equities over 10 years. So right now, that loan is like free money from an investment returns perspective.

When people are in debt you can’t always use the ‘pure math’ comparison. The reason is that someone in debt will use the money in other ways if they don’t pay off debts. For example, if Hope doesn’t pay the student loans she’ll spend $1500 on a bridal shower. Most likely any other income will go to trips. Especially if you’ve been holding student loans for well over a decade and the balance has hardly budged, I’d get those of the table myself.

I don’t think I’m really just advocating for a “pure math” approach for Hope. I’m discussing the different sides from which one can consider this low interest loan.

If Hope is going to spend her income on trips/discretionary anyway given her overall financial trajectory, then paying this loan or not will ultimately make no difference. That a person in debt will spend money on other things is actually the reason for Ramsay’s Step 0: No New Debt. Without this you aren’t even at the point where you pay off any debt, let alone debate over super low interest debt. Because without Step 0 a person in a debt-driven lifestyle will eventually wipe out the gains of payoff with new debt.

I am 100% committed to NO MORE debt.

talk is cheap. What are you doing to achieve this? You talk of living within your means but you seem unable to describe what your means (meaning income) are in a meaningful way. I can’t believe you when you just say things like this anymore.

This exactly. Hope has shown time and again when she has money she spends it. Might as well spend it getting out of debt. Those loans have to be at least 20 years old at this point.

She started in March of 2014 with $31,687 of student debt. 21 years later she has a balance of $19,036. That being said in 21 years she has paid $12,681 or the equivalent of about $50 monthly. I want to continue to be hopeful that next month she will get below $19,000 and her savings will be above $6000. The trick is for that debt number to go down and that savings number to go up and to be able to live on what she has while those two things happen. She is blessed to have the circumstances she has but at some point she may not be able to rely on her parents opening up their home to her. Housing is 30% or above for the majority of renters that I know in terms of income.

You are right. I graduated with my masters the same month I got pregnant with Princess. And she just turned 21.

Not sure why you even bother to ask readers where to put $600. Your income and expenses are wholly missing from the equation which makes everything a moot point. In the last post you glanced over $5,000+ in missing spending from the house proceeds. This is in addition to the mysterious $4,000 increase in credit card debt in the 1-2 months before the house sale. I hate drag up the past, but you also did the same 1-2 years ago with some significant debt due to your BF that you hid. If you can just overlook many, many thousands in spending, I’m not sure debating where to put a couple hundred dollars is going to help you at all. This is a decades-long pattern you need to break if you ever want to be in control of your life again. You had the greatest gift of gaining and cashing out a huge amount of equity in a few short years. And you squandered like 30% on unnecessary and/or unknown things. Yet, you keep insisting you’re breaking free from your spending patterns. I would argue you are doubling down. Any time big income comes in or there is money in your savings account you always find something to spend it on, and quickly. Sure you have savings at this minute, but your patterns and mindset have not changed so I’m not confident that it will last.

The majority of your Ally categories are just savings buckets to be spent by the end of the year (christmas, vacation, occasions, etc). So putting it in Ally is essentially just giving the okay to spend it in a few months on a roadtrip or the wedding. You have no self control with money. I think the only way you would succeed is to have a HYSA account that you are not allowed to touch (i.e. under your sister or dad’s control – yes, this is extreme and I understand why you would feel insulted). Or to be very diligent in sending savings or extra income IMMEDIATELY to an account you absolutely cannot access like a 401k account (NOT ALLY) or to student loans.

I agree 100%. I believe Hope is close to, if not already, a bona fide candidate for something like a spendthrift trust. It’s going to take a lot less talk and a lot more action to change that.

I don’t want to be saying this is a hopeless situation as far as maintaining financial independence, but it’s hard not to conclude some catastrophic intervention in the near future…

The other thing part of me doesn’t want to bring up but seems like a realistic trajectory is maybe it’s time to start pursuing disability. That is a long road and approval may not be possible today, but maybe that is the best realistic glide path.

Basically I’m thinking maybe it’s time to plan for an outside-regulated, cash-based existence. It’s hard to hold on the trust in managing assets or reserves anymore.

Okay I’m feeling bad now about being too harsh. I guess I got triggered by your vague idea of “getting 10k in Ally” combined with all your rash spending over the past 3 months.

I 100% believe you need the structure of bucketed savings for non-regular expenses. And Ally seems to fit that well for you. Your income should be funneled into these bucketed accounts on a monthly basis (at minimum). Extra income above what your budgeted spend is should be directed to emergency and house fund savings. This bonus would fall under that category. So I pause when you say you’ll “send it to Ally” because with the way you have it structured that could mean anything.

I think you would do better if your emergency, house fund, and future car savings were at a completely different bank than your bucket budget categories. A bank you never log in to once you hit your target. Then only do push transfers externally from another bank website whenever you have excess to save and need to transfer money in. Reason being, is your money journey has been highly influenced by your emotions. When you are in a bad place emotionally you spend money frivolously on things you get value from, like family trips. When you are in a good place financially, you get a real high off of knowing you are doing a good job and have extra money. And on that high you end up committing to large expenses (cars, celebrations, trips). I’m afraid that once you save 10k for an emergency fund, you’ll still see that big total number every time you open up Ally. Then you’ll ride that high of feeling flush on cash and start coming up with ways to spend it and feel completely justified about doing so.

You need to get yourself into a place financially where you feel safe by knowing you are actively funding and covering your monthly and irregular expenses. But you also need to trick yourself into a place where you still need to hustle because you don’t feel flush with cash and start frittering it away. By physically separating these accounts you will hopefully not be tracking exactly how much you have saved in the longer term funds (past 3-6 months of expenses) thus reducing temptation. It sounds pretty crazy written out that way. Because who wouldn’t want to know their savings progress? But it could be what you need to break your constant high/low emotional spending cycles.

I’ve actually had the same thought with regards to the Ally buckets.

After a ENT doctor visit next month, I’m really going to have to make a decision on a new pair of hearing aids. And taking $2-5K out of that account is just not something I want to do. Same for travel/Christmas, etc.

Will put some thought into that. It is very motivating to watch that account grow weekly. And touching is not something I want to do. A different account makes sense.