by Ashley

Friends – it is the end of an era!

I’ve been blogging here for more than a decade. It’s absolutely bonkers to me how our financial picture has changed during that timeframe.

Where I Started

When I first started blogging here, I had twin two year old toddlers and I taught adjunct online part-time for peanuts. We lived in a tiny duplex complex in a scary part of town in a place that had no air conditioning (living in Tucson, AZ where it’s frequently in the 110+ temps during summer!)

Life felt tight. Financially, emotionally, all of it.

What Changed Along the Way

Over the years, life didn’t just change – it evolved in ways I never could’ve predicted.

There were several moves. First from the duplex to a better rental, then to the home my now ex-husband and I bought together, and then back into a rental mid-divorce with twin 6-year-old kindergarteners.

I landed my first “real” job for $55,000/year (and felt rich!). I climbed the ladder, got raises, and carved out a space for myself professionally.

I re-married, bought a home with my new husband, and have started to travel the world (to Peru and Indonesia with work; to Italy and Hawaii with hubs in the past 6 years).

But despite all of the changes, I stayed very consistent with my finances.

I’ve driven used cars. I’ve invested regularly. I’ve shopped frugally. I’ve lived below our means.

The Long Road of Student Loans

And then there were the student loans.

When I graduated in 2013, I had over $100,000 in student loan debt.

In my oldest debt update post on the blog (June 2014), I had over $96k.

For years, that payment was one of my biggest monthly bills – second only to housing.

I chipped away at it consistently. Even during the federal pause, when payments and interest were suspended, I kept going. I doubled and tripled payments, trying to take advantage of that window.

Eventually, I made the switch to the Public Service Loan Forgiveness (PSLF) program.

I started qualifying in August 2015.

And in March 2026, I made my 120th qualifying payment.

I submitted my paperwork. And then I waited….

The tracker said: “Congratulations! Your PSLF form has been accepted!”

It sounded promising…but also vague enough to make me nervous.

It took another 3 weeks…

But just last week I received official notification:

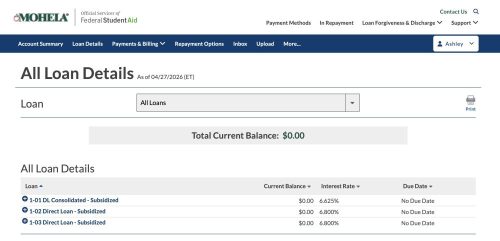

MY LOANS HAVE BEEN FORGIVEN!

The balance is now $0 for my remaining student loans.

What This Really Means

Yes, this is huge. But the bigger thing?

I’m officially debt-free (minus the mortgage)!

For a long time, student loans were the last thing left.

When I first started blogging here, I had every debt you could think of – credit cards, store cards (e.g., Mattress Firm), medical debt, car loans, and even legal debt.

The accountability of blogging here really helped me, and I was able to pay off a lot of debt in a short time. But my divorce set me back a bit financially for awhile. I was debt-free minus student loans way back probably 8 years ago? And then that slipped for a time when I had lawyer fees and another car debt added to the mix. I worked hard and paid those off and was back to just the student loans for at the past 3 years now.

A Decade Later…

Now here we are. No credit cards. No car loans. No student loans. No medical debt. No store cards or other lines of credit. Just a mortgage. And a completely different financial life than the one I started with those 12 years ago as a newbie blogger at this little get-out-of-debt blog.

If You’re Still In It

If you’re earlier in your journey to get out of debt, here’s what I want you to know:

It doesn’t happen all at once. It’s slow. It’s boring. It’s nights at home and inexpensive get-togethers with friends. It’s not linear. There will be backward slips because that’s just the nature of life. It’s sometimes discouraging. But consistency outweighs intensity. If you stick with it…it works. You don’t have to be perfect. You just have to keep getting back up whenever you fall.

For Long-Time Readers

Thank You! Truly, sincerely, from the bottom of my heart. I wish I could take you all out to lunch or coffee or host a get-together at my house. It has been your advice, your tough love, your words of encouragement, and your wisdom that has helped to get me to this place.

You know the saying that you don’t know what you don’t know? There are so many times that YOU ALL taught me things I didn’t even know I didn’t know! You’ve been my virtual friends and financial confidants and advisors over the years. And your generosity in offering your wisdom to a total stranger, and for FREE, well, it’s enough to bring tears to my eyes. Thank you.

What’s Next?

No one knows what the future holds, but for the time being, I’m going to stick around. I’ve asked a couple of times what you all think…should I be done when my debt is gone? And several folks have commented that you’d like to keep seeing my posts as I work toward my FIRE goals (early retirement!).

That may change down the road, but for now I’ve really enjoyed this little online community and I’d like to stay a part of it!

A Quick Reality Check

I also want to say something that’s been on my mind. From the outside, my life today might look like I “have it all.” I have a good job, a high salary, a beautiful home, I travel regularly, and have financial stability.

I won’t downplay it. I DO have a lot, and I’m incredibly grateful.

But this life wasn’t just handed to me. When I had my twins, we were living below the poverty threshold (yes, literally). I was scraping by, making my own baby wipes, juggling childcare, underpaid for work, zero local support (emotional support, yes, but not physical or financial), and a whole lot of stress. Everything you’ve seen here has been built step by step, over years.

So if you’re in a hard place right now, please don’t assume you’re behind or that this kind of progress isn’t possible for you. It is.

And at the same time, it’s a good reminder for all of us not to judge someone else’s situation based on what we see today. I’ve had people describe my life as “bougie” or assume it’s rooted in privilege.

Maybe it is, now.

But it’s also something I bought and paid for with my own grit, determination, and hard work. I earned it with my blood, sweat, and tears across many years of perseverance and difficult seasons.

And while everyone’s path looks different, meaningful change IS possible over time. You just have to keep going.

Thank you for being my cheerleaders, my confidants, my reality check, and my sounding board. I appreciate you more than you know!

Hi, I’m Ashley! Arizonan on paper, Texan at heart. Lover of running, blogging, and all things cheeeeese. Early 40s, married mother of two, working in academia. Trying to finally (finally!) pay off that ridiculous 6-digit student loan debt!