by Ashley

We’re now in Month 2 of our financial experiment where I give my 13-year-old girls $100/month and they are responsible for buying ALL their own clothes and makeup, plus any “fancy” toiletries (I will continue to buy all their basic necessities).

I appreciate the comments and feedback I received on my last post when I shared our experiment. I updated the contract I shared with the girls to clarify I would cover ALL basic necessities (e.g., face wash wasn’t originally listed; and the contract said floss OR mouthwash when I really meant floss AND mouthwash, etc.).

The day I gave the girls their first $100, we sat down together and worked out a budget. I told them that we typically spend for back-to-school clothing shopping ($300) and what they might budget for summer time clothing (including swim suits, flip flops, etc. approx $200).

We had a rough timeline

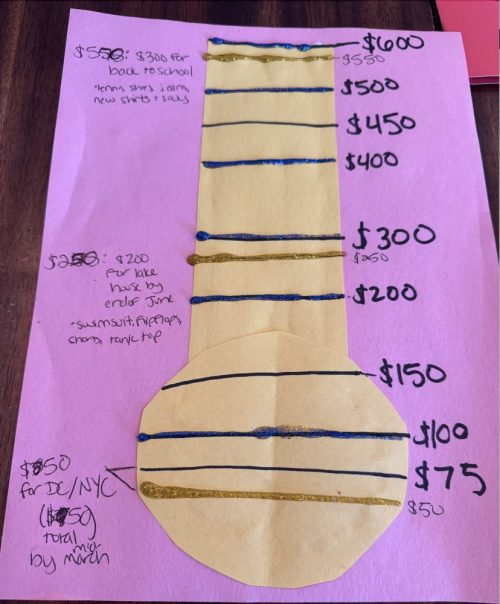

We need $200 by May/June for a summer clothing haul, and another $300 by July/August for back-to-school.

From there we worked backward.

We have 7 months from Feb-Aug, which is $700 worth of money; but we need to set aside $500 of it for these planned expenses. That leaves $200 for makeup/skincare and fancy toiletries or other clothing incidentals between February and August. That’s only about $30/month!

I think this was a bit of a shock and also helped them to adjust their thinking a bit.

For instance, both of them wanted to buy new clothes for our D.C. and NYC trip. However, we have LOTS of clothes that fit and will work well with the colder DC/NYC weather (it’s already summer-weather in Tucson!). I encouraged both girls to try to make outfits from their closet for the DC trip and maybe just purchase one or two new things instead of a whole new wardrobe for the trip.

This worked great! Daughter 1 spent $15 on a shirt and called it good. Daughter 2 didn’t spend anything in the month of February, but has $50 budgeted for DC/NYC (to be clear – this is money budgeted for clothing in preparation of the trip. She won’t have to spend anything on the trip, itself).

My reaction

Honestly, I was a bit shocked at how maturely the girls approached the situation. My past experience with them is that when they receive money or gift cards for birthdays, it’s like the money is burning a hole in their pocket and they “need” to go shopping STAT! I expected this to be a similar experience. But, if anything, they’ve done the opposite! They’re saving their dollars so they have well funded accounts for their summer and back-to-school hauls.

Also – we had so much fun together “crafting” – the girls made a savings thermometer! Remember when I used to make debt thermometers to track my debt payments!?

Side Note: We realized after creating it that we probably should have created two separate savings thermometers – the first for summer and a second for back-to-school because they’ll save and then spend so it doesn’t make sense to have the two savings goals on the same thermometer. Oh well. It was a fun project and a learning experience.

I did have Daughter 1 tell me last week that she needed some new concealer and when I encouraged her to use her money to buy it, she decided she could go a bit longer with her current concealer. I like that they’re becoming thrifty (using every last drop!), but I will definitely encourage her to continue to use her budget to buy the things that she needs as the needs arise – that’s what the money is for!

This also brings up a comment someone left, saying they were worried that teens would prioritize the wrong things and would never buy themselves new socks or underwear, for instance. I’m planning to stay closely involved and will help guide the girls to make these types of decisions and not put off needs in favor of buying more of the “wants.”

So far, So good

One month in and, so far, I’m really pleased with how well the girls have done! It’s gone better than I’d expected!

They received their March budget and things are going well this month too! I’ll continue to monitor the situation and we plan to have intermittent check-ins to make sure everything is going okay and make decisions about whether any budget modifications are needed, etc. This is intended to help teach the girls to budget – not be punitive in nature. So if it’s really not working out, I’m happy to step in and make adjustments or help as needed. But so far I’m really proud of the maturity they’ve shown and how well things are going!

I’ll give an update in a few months (e.g., maybe after the summer shopping trip) to report back on how they’ve done on their savings goals and how things are going with this financial experiment, in general.

How much financial responsibility do you think is appropriate for teens to manage on their own?

Hi, I’m Ashley! Arizonan on paper, Texan at heart. Lover of running, blogging, and all things cheeeeese. Early 40s, married mother of two, working in academia. Trying to finally (finally!) pay off that ridiculous 6-digit student loan debt!