by Hope

I received a lot of great feedback on my longer term savings plan a month or so ago. Specifically about how having all my “buckets” on my Ally account may make me more susceptible to dipping into these funds. And that made complete sense to me.

So I’ve reallocated my Ally account to be my long term savings account only. And left 3 buckets there. (I didn’t remove any money, just moved everything I had been putting in the various buckets to the Emergency bucket.)

Savings Plan

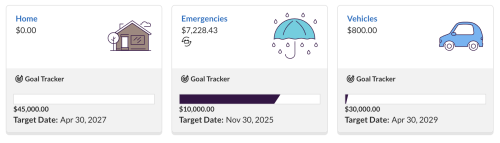

Here’s my buckets on this account, goals and hoped for timelines:

Goal #1: $10K in my emergency fund. I should hit this next month or October latest.

Goal #2: $45K by April, 2027 toward a home. Or rather toward land for my next home. My dream is to build a small home, cash flow it. And by build, I mean with my own two hands plus some help from family, kids, etc. My sister has the same plan. But this initial money will be used to buy the land in cash, paid in full. No debt.

Goal #3: $30K by April, 2029 toward a new car. I don’t see any reason my car should need to be replaced before than barring anything catastrophic. This is in preparation for paying cash for my next car.

Sinking Funds Where?

I have a bunch of other savings categories in my budget. Now I have to figure out the best vehicle for those. Suggestions? (And yes, I am working on a revised budget now, will share for feedback in the next week or so.)

The commenters were spot on in making the recommendation for me to split these longer term savings buckets from those that I will need to dip into more often. But there do I keep my other buckets? I would love your thoughts on that.

Hope is a resourceful, solutions-driven online business manager with over two decades of experience helping clients streamline operations, manage projects, and grow their businesses through digital marketing and technology.

But life has a way of rewriting your plans.

A year ago, Hope made the decision to move in with her aging parents full time – a season she wouldn’t trade, even as it came with its own financial and emotional weight. Earlier this year, she lost her mother, and is now walking the tender, disorienting path of grief while learning what “forward” looks like from here.

Hope came to the Blogging Away Debt community in 2015 as a single mom raising five foster and adoptive children. She’s written through job changes, financial setbacks, and the bittersweet transition to an empty nest. Her kids are finding their footing in the world now – and so is she.

Rooted in faith and fueled by the same perseverance she’s brought to every hard season, Hope is ready to face her finances with fresh eyes and an honest pen. She believes that clarity, courage, and community can change the trajectory of anyone’s story including her own.

She lives in Austin, TX with her dad, loves adventures with her dog Addie, and is figuring out, one step at a time, what this next chapter is meant to be.

I am a fairly new reader, so perhaps you have touched on this the in the past, but in your budgets and debt/savings reports I do not see a retirement fund category. I have to assume that you have some money saved somewhere for retirement – if not PLEASE add a category for that before buying land and building a tiny house! I also hope you have had jobs that will allow you to have enough credits to have at least some social security benefits!

Hi and Welcome and thanks for the comment.

Retirement savings has definitely been one of my failures. But yes, I do not have a retirement account, two in fact, that are funded weekly. It’s not a lot by any means, but it grows weekly now.

And yes, have working full time/part time W2 jobs throughout the years so I will qualify for social security benefits…if they are still around.

Last paragraph- sinking funds go in a savings account. SF for most people must be liquid as they are generally spent within the year. For your situation, the only thing that really matters is that you are tracking them so you know each SF is funded according to plan and not being double counted. Whether that is buckets, separate accounts, or a spreadsheet that breaks down the balance.

I’m going to push a little bit on the semantics. Sinking Funds function differently to Savings Goals. Sinking Funds are for things that are certain to need payment, just not on a regular monthly schedule. Savings Goals are for things you can delay or seek alternatives to if needed. Sinking Funds must be funded before you allocate to Savings Goals. I do agree with the critique of your past approach to bucketing categories, but I’m also concerned that you regard SF categories as the same as a savings. To me this equivocating of categories you NEED to spend in irregularly with goals you WANT to fund is also a dangerous thought process. I think historically you have kind of thought, oh I have a savings and you raid funds that needed to be earmarked for lumpy expenses.

Hope,

You sold your house because you didn’t want to maintain it. Now you are going to build one?

You need to be honest with a therapist about what is changing to make you able to take care of, much less build, a house even though you hated home maintenance before.

And I feel bad that you are so comfortable forcing kids to help you. You say they are launched, but you keep depending on them and blowing money you don’t have on them. That five grand that mysteriously disappeared and was spent on kids could have been a down payment on something.

You even had issues mowing your own lawn! What are you thinking? There was the push mower, then the electric mower… at one point you had someone’s boyfriend mowing it.

Are you doing all this because if you make them to help you they won’t move forward without you?

What’s really nice about my relationship with my kids is that I don’t have to “force” with my kids. They want to see me, they want me to visit them, they want me to stay with them. I don’t know what it is about your experience that makes you look at my life through a lense of “forcing something on my kids.”

Two of my kids have already claimed the right to move my stuff to wherever I move to next because they want that adventure. All of my kids are excited at the thought of being hands on with a tiny house build. We love remodeling our home.

We just enjoy being together. There is no force to it. Their life, their choice. They just choose to spend time with their mom. I’m sorry that’s so foreign to you.

I think we’re just trying to figure out why there is this pattern where your relationship with your kids is the reasoning/excuse for two issues:

1. Unreasonable sums of money spent on visiting or traveling with the kids, or simply is spent on them without much logical explanation. This has been done at great detriment to your own stated goals and your basic financial stability.

2. Your kids are conveniently offered as the reason why you don’t plan to do or pay for something, to an unreasonable degree. Just because you claim they are excited to do it doesn’t mean you’re not also relying on them for your plan to work.

If the relationship is truly just that you all love being together and you’re so happy and supportive, why has it been this insane money sink from you over and over?

It’s just not going to hold much water to read you write how they are excited to volunteer for you; when at the same time, they see the choices you make and know you have this ambitious plan that obviously requires assistance. You have arguably been the largest influence on your children’s psyche and decision making, even as adults. Does it make sense that all the accountability externalizes to them for why they come to you the way it has and the way you expect?

It seems like you keep changing your goals, your buckets, your finances.

You ought to choose a basis of presentation and stick with it for at least 6 months. It can be as simple as the 3 above [house, emergency, car] with 1 addition: “Funds for Irregular Expenses” which has to include insurance, auto maintenance, whatever else] or more categories, but whatever will work for you and **which you will stick with for at least 6 months**.

While you’re at it, there is a revolving view of what accounts are shown or not (investments, second savings account, etc). Choose a baseline and stick with it. If you exclude them from reporting, then state the balance once, and resolve to never withdraw or borrow from them without blogging about it and justifying it – preferably ahead of time.

Finally, your debts baseline should not start at Oct 2023. It should start at May 1, July 1, Sep 1, whatever. But it needs to not be so out of date and obscured by your one-off windfall.

You are right. I am evolving, my dreams and plans changing. I reserve that right.

And I still have absolutely no idea where I want to live once I am done here.

The only thing I am really consistent with is the need to be in a better financial place, thus savings and paying off debt.

But my next phase…absolutely no idea what that will look like.

So let me get this straight. You couldn’t handle the maintenance of a home or yard when you owned a relatively small house/lot in Georgia so you just had to sell it, but you’re going to be building a new small home on land with your own hands? Make it make sense. Who will maintain all that?

All that? The 300-500 square foot that I will be intimately familiar with from building it? Me.

My home was over 50 years old, on a lot that had major water issues. You may not be familiar with that aspect. But it was a lot.

This home will be built very specifically to my needs as I age, my hearing goes, and easy access to maintenance requirements.

I think these savings buckets with goal dates are great but are they actually obtainable? You would need to save over $2250/month minimum to meet your first goal of $45k by April 2026.

This is over $77k in 3.5 years…

This is not reasonable, Hope. One of the reasons your plans fail is because you don’t create SMART goals.

SMART = Specific, Measurable, Achievable, Relevant, and Time-bound

In this case, this isn’t achievable unless you win the lottery and designate a trust to secure your money away from yourself. That exhausted phrase about the definition of insanity – “doing the same thing over and over and expecting different results” – that’s you.

This is expecting yourself to save 1/3 of your take home pay, assuming you can even secure stable income, after never being able to save even 10% of your income.

I think it’s time to set money aside so that you have no access to it, as “emergencies” will always arise. But first, ask for some professional help about what is reasonable to be able to save.

Do you have the skills and ability to build a house with your own hands? Will your kids, who live all over the country, have the time, skills, and desire to help you build a tiny house? Realistically, how much help would your friends and family provide? I want to see you succeed, but you need a realistic goal. I do not think this is one. Perhaps a small piece of land and a mobile or small manufactured home would be a better goal.

Lisa said exactly what I was thinking. My family built a house when I was growing up. My dad had extensive experience in construction and it was still a huge project and we had to hire different tradespeople, otherwise it would’ve taken forever. This feels like another example of being more of a dreamer than a realist. A mobile home would be a far better option for someone without the skills/time needed to build.

I think Dreamer is a nice spin on it.

It’s find to dream if you aren’t affecting anyone else. But this constant reliance on dad and kids for a roof, food and crashing whenever she feels like it is pushing that dream on other people.

And at 50, reality should have set in a while ago or retirement is going to be completely reliant on others as she hasn’t maintained a plan for that.

I was taught it’s great to have dreams…if you can achieve them without relying on the fruits of other’s labor.

We built several of our homes growing up too. And two of my children have experience building tiny homes specifically. Two of my brothers work professionally as handymen. And my dad is an electrical engineer by training. There will no doubt be things we (my sister and I are both doing this) will have to hire out.

But we all agree that if we can cash flow the land and the homes, taking the time we need, it sets us up for success down the road.

Is this a joke? How long ago were relishing in the “freedom” of living in your car? Laughing at those who told you that you’d want a house again and were short sighted in selling the house? And you, with no experience, expertise, know how, patience, or any sort of relevant skills, intends to build a whole house from scratch? Tiny or not, this is a huge undertaking. When are all your family and friends going to help you do hard manual labor? How do you intend to compensate them? You couldn’t do even run your own household without significant debt and you’re intending to project manage a building site?

So I ask again, earnestly… is this a joke?

Guys,

Hope is wanting a tiny house on this lot. She has said that many times before.

There is a huge difference between having to maintain a large house vs a tiny house. There is also a huge difference between maintaining a brand newly built home vs one that is 100 years old.

When it comes to mowing/outdoor work I would argue she makes plenty of money to hire someone to do this. Most elderly people do not mow their own lawns.

I do think funding retirement is important…but that does make the assumption that one expects to survive into retirement. Some people simply work at least part time their entire lives. She has also said she will be looking at an inheritance. There is something to be said about focusing on your kids today vs yourself 20 years from now. That’s a moral priority question that a lot of people give her hell about. If you had her priorities you might choose differently.

Her only debt is her student loans now and her interest rate on those is very low. Now is the time to focus more on future planning and saving. She’s making progress give her credit where credit is due.

That being said Hope, I do believe you could realistically save 1/3 to half of your income if you keep paying the min on your student loans (which unlike some people I would advocate you doing). Don’t blow it because if you don’t do this, 10 to 15 years from now you will regret this assuming you are still around then (which we all know is never guaranteed).

oh come on. She did not sell a large house but a modest house, nor was it 100 years old. From the 70s as I recall.

Re retirement, she is already deaf now. How is it gonna be in 15 years? She’s overweight and goes to a chiropractor instead of getting actual medical care. She’s not going to be able to keep working.

as the kids say “bffr!” Even if Hope made enough money, she unfortunately does not manage it well enough to be building a home herself and buying a plot of land if she continues on this path that she has been on for quite some time. And for most anyone building it with their own two hands would not even be feasbile, they will need contractors for electrical, plumbing etc. She has been told don’t blow it many a time, by many well intentioned folks here.

You mention she mentioned an inheritance. No one can ever count on an inheritance. And as someone who has dealt with a family member that has needed to be bailed out financially their entire life, she could be in for a very bad surprise when any monies are doled out. Her family may have decided she has gotten her share already and made provisions that funds are allocated elsewhere. That is what our family has done. I hope she is not factoring any future possible inheritance into her financial planning. Residential Care, if needed, is over $12K month (in my VHCOL area, so may be less there) and 8 hr a day care givers are $40/hour. If someone in the family needs more care later, any funds they have could be used quite quickly.

Yeah, in a tiny godawful town like where I grew up, my parents’ assisted living was about that much 10 years ago. It’s insane.

I noticed there are tiny houses for sale on Amazon. Have you looked at them, Hope?

We have! Dad sends my sister and I all sorts of information on them. We (all 3 of us) watching tiny home shows on tv when we are together. It’s a constant source of research and entertainment for us all. There’s even some tiny home villages here in Austin that my sister and I plan to go visit.