by Hope

My focus is split – student loans and savings. I just updated you on my debt load after payments made this month. Now it’s time for a savings update.

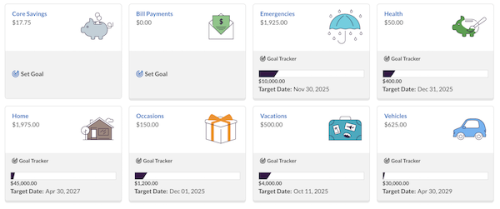

I currently have a total of $6,249 in my personal savings accounts. $807 is in my long standing personal savings account. And the rest is in my new Ally savings account assigned to all my savings buckets that I created when I created my budget. There was original (post house sale $4,000 more in savings. I will explain use when I get a May finance update together.)

How do you like Ally?

I am so grateful to the person in my comment about a high yield savings account who recommended Ally. I LOVE, LOVE, LOVE the buckets and related goal and date feature. And then seeing cumulative total is very motivating.

It’s been so easy to set up and use. And feels “far away” so I’m not at all tempted to look at it often let alone touch the money there.

My only complaint is that transfers take anywhere from 3-4 business days. While they take the money out of my account on day 1, they take 3-4 days to deposit it into my account. (Even if they listed it as Not Available). They do show the transfer as pending, but seems like a stretch to take that long to even record in my account.

I only have the single savings account. And I’ve already earned just over $17 in interest. And that’s in just over a month. Woot, woot!

Very motivating.

Future Plan

The plan remains the same, with a small hiccup of this unplanned stay in GA while Beauty and fiance recover from 4 wheeler accident.

I will continue to live with my parents, helping care for my mom (and dad as needed) until I am no longer needed. Things are working well with dad. I take care of day time care – feeding, bathing, and changes. And then cook several times a week for dad and I, eating leftovers in between. Dad handles evening care and is free to get out of the house during the day. We are both quite happy with this schedule.

And I’m able to work around mom’s schedule, and vice versa. I start at 4:30am daily. And we make it work. I am diligently saving and paying some extra to my student loans every month. But I think I am leaning slightly more to saving.

My siblings have stepped back in while I am here in GA.

Hope is a resourceful, solutions-driven online business manager with over two decades of experience helping clients streamline operations, manage projects, and grow their businesses through digital marketing and technology.

But life has a way of rewriting your plans.

A year ago, Hope made the decision to move in with her aging parents full time – a season she wouldn’t trade, even as it came with its own financial and emotional weight. Earlier this year, she lost her mother, and is now walking the tender, disorienting path of grief while learning what “forward” looks like from here.

Hope came to the Blogging Away Debt community in 2015 as a single mom raising five foster and adoptive children. She’s written through job changes, financial setbacks, and the bittersweet transition to an empty nest. Her kids are finding their footing in the world now – and so is she.

Rooted in faith and fueled by the same perseverance she’s brought to every hard season, Hope is ready to face her finances with fresh eyes and an honest pen. She believes that clarity, courage, and community can change the trajectory of anyone’s story including her own.

She lives in Austin, TX with her dad, loves adventures with her dog Addie, and is figuring out, one step at a time, what this next chapter is meant to be.

Am I reading correctly that $6,259 is all that is left of the $50,000 you cleared from the house? The credit cards took half of that, and I know you paid back your Dad and had some moving expenses, but where did the rest go?

Is there a post in the pipeline about your income? This and the debt post are not really actionable without knowing what’s going on with income.

My income is still highly volatile. I may make $3K one week and $60 the next. Until I get a buffer to live on last month’s income again.

But goal is savings and debt first for now.

My monthly obligations are pretty low.

Hope, you have to know by now this response doesn’t make sense and it doesn’t work, no matter how many times you have tried it over the years. There is no debt payment or savings without income. There are no expenses without income. It does not matter that it is sporadic or volatile. Nothing you say about what you will pay or save holds weight without information about how income flows to your goals.

“Until I get a buffer to live on last month’s income” is the income equivalent to “May doesn’t count.” You must track volatile income and be intentional about how you are applying it to expenses. Handwaving that sometimes it’s low and sometimes it’s high is a major factor in your debt cycle. You can no longer afford to sit tight until you can get on a last months’ income buffer. Use a variable income method now.

Unless you end up on disability before then, you are looking at >10 years before you can access Social Security and Medicare. You will be so much better off to deal with variable income starting now.

I get what you are saying. I didn’t think through the last month’s income buffer when I created my budget.

So right now I’m just hitting each budgeted item as income comes in. Thankfully I have very, very little monthly overhead now.

But I may need to stop my savings and build up that one month buffer and then resume.

Will think about that once I have a minute to sit down and think things through. Right now, I’m full time caretaking and trying to maintain my current workload. It’s all I can handle right now.

You’re starting to get on the right track here, keep going. Same advice on the savings goals as I gave on your post-house budget post(s) in that you are getting ahead of yourself with the savings goals. I said then you need to fund the emergency fund before allocating to savings goals. With the unpredictable income, step 0 is actually to fund the low weeks from the high weeks.

If your method is just paying things when the money comes, you won’t know if your high week spending is shortchanging your low weeks. Debt accumulation is inevitable with this approach.

Totally understand that caretaking takes a lot, but you are in a dangerous position right now. You are back to a negative net worth and all evidence points to burning through the last of your liquidity. You don’t have much left to burn before you’re toast.

Yes, I’m getting that. I think I need to pause the savings and extra debt payments and get a 1 month of spending in the bank so I can live on last month’s income again.

Having a highly changeable income is no excuse for refusing to track it. As a private contractor, I watched every PENNY because of the variance.

We know you can do basic math so it’s confounding as to why the simple Money Made vs. money spent never shows up on your page.

And you are saying May didn’t count? Well, if it’s on a credit card, then June won’t either.

I said May didn’t count because it was so out of the norm…house sale, debt payoff. It didn’t fit into my planned budget.

But don’t worry, the posts are written and scheduled to explain May.

I always track my income. I have to…taxes, ss payments, etc.

This is the first time in a very long time that I’m making more than enough to cover my monthly bills without having to borrow from Peter to pay Paul or whatever the saying it.

I am a work in progress.

Hope,

So the first time you don’t have to worry about income meeting expenses is when you live free with your parents?

You are fifty. Thats’ not a lifestyle choice it’s scary.

I know you say May doesn’t count- but most adults count paying rent/utiilities as a basic of adulting.

And am no longer the sole support of a family of 6. Yes. The kids are all financially independent. Princess even got her first paycheck this week.

Ya’ll just can’t let go of that flippant statement. I am explaining May in a series this month.

That statement was made in repsonse to people saying that me adding the cc payments to my budget tracking sheet confused them.

I was just trying to track all my income and all my output in one place.

But May was an exception because of the house sale and debt payoff.

You aren’t, and have never been, the single provider for a family of 6. By the time beauty moved in with you, the twins were paying 3/4 of your mortgage as rent for the living room….and for you to be complaining they were playing video games in their free time.

You are correct. Once the twins were out of school for 6+ months, they were required to contribute financially to the household. That was the case with all of my children, if they were still living at home. Beauty paid rent at some point. And Princess and Gymnast never lived at home after they finished school.

But to clarify, the amount of “rent” was never applied to a mortgage as I was still renting when the twin’s were still in the house. And when they did move out, the “rent” paid for their application fee, deposit, furniture, and even stocked their fridge and freezer. And when Beauty moved out, part of the rent she had paid stocked her kitchen and supplied much needed items for her new home.

All of my kids lived by and received the same support, it just looked different based on their life choices. School or trade school, cash car or nicer car, new phone or trade in phone, etc. These rules were established long before they applied to anyone. Everyone knew the support that I would provide based on the choices they made.

I am with Laura, you only have approx $6200 left of your $50K? That is rather horrifying. IF you truly want to make changes and move forward with integrity on this page, you need to be 100% transparent with what was owed and where it all went, even if it is embarrassing. If you don’t feel like you can do that, I really think this is not a great spot for you. You may be out of credit card debt at this moment in time but I don’t see that lasting more than 1 month to be honest. If you are not honest here, where you can go back and see the implications of your past decisions, how can you do better next time? So many people on this page have “called” the inevitable every time you make a poorly thought out decision and then when it comes to pass, you seem to say “oh well, I should have listened”….

She’s not interested in feedback and ideas. She makes decisions, spend money, then post about it after the fact. Then there’s her poor writing skills and/or utilization of AI and purposeful obfuscating of things, which further muddies the waters.

She’s not in it for transparency. She’s not here to get out of debt. She’s here for whatever pay she gets from it. One of her “hacks” for income, but here we are with her still 20 grand in debt, 20 grand missing from the sale of her one asset, and no meaningful income. All while the site owner AI bot tells her “good job on paying that debt!”. It’s ridiculous.

She should be completely terrified. I’d hope that she has no illusions of ever retiring, but I think the more likely outcome is that she ends up sponging off her kids like she’s sponged off her parents on and off for her entire adult life. People in her life need to start telling her “no”. Let her live with the consequences of her actions.

Need a like button for this post. Hope won’t answer any questions just ignore.

Jen – I completely agree! She should be terrified. Like I commented to her several weeks ago, I have a paid for house, a great job, savings and no debt and I’m scared of the ‘what ifs’. It hurts my chest to think about the situation she’s in.

I’ve got a planned series for July…where the house proceeds went. Stay tuned.

So my question is this? Where did $21k go in 2 months?

51660 (House Proceeds) – 600 (Painter) – 21000 (Credit Card debt) – 2600 (Dad Furnace) = 27,460

27460 (Remaining Proceeds after sale) – 6249 (Savings account) = 21,211 leftover

I wonder what this statement “There was original (post house sale $4,000 more in savings […]” means…

Best case, she paid $4,000 extra toward student loans.

Likely case, she took out $4,000 for a specific undisclosed item or series of undisclosed charges on a credit card. Which she may explain if she writes a May spending post.

But remember, May doesn’t count!

Hope seems to think that if she doesn’t track her spending, it doesn’t exist.

Well, given her lack of income accounting, maybe that doesn’t count either.