by Jim

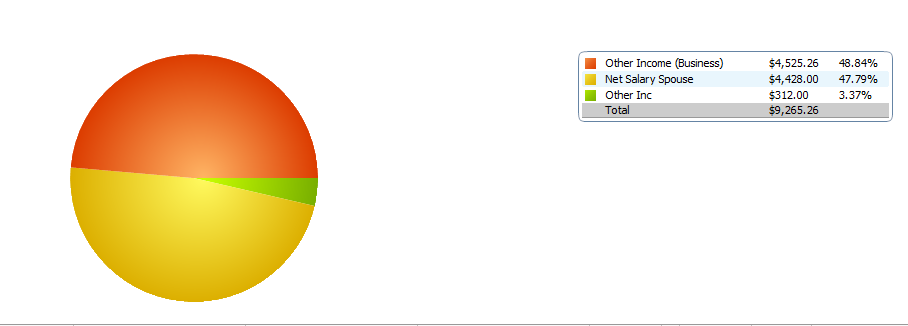

Before I start I just want to point out that this graph above me and the table that will be below this will not match up. The reason for this the table reflects both my auto totaled out payment as well as my income tax. Now the table below is My Income/Expenses Year to Date On Broad Categories. The reason I putting this up here is to see where I can improve on the most. I have printed out right next to me My Current Spending vs Average Spending where I compare this month to Sept. 1, 2013- Feb. 28, 2014. So that will be the second table. As I started doing the table, I don’t think I will be doing this table again, it is very strewed (I think that is the word I am looking for)

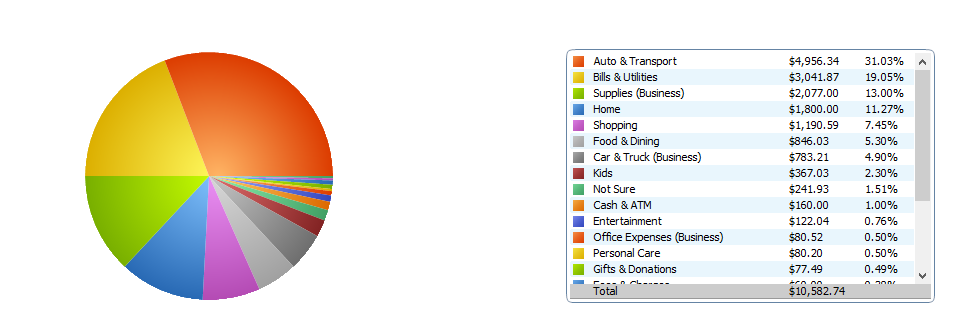

[table “4” not found /]Let’s point out somethings to note. The reason my Auto & Transport is so high in February, that is when I put the down payment on the Van. For some reason I have putting gas in two categories Gas under Auto & Transport, and in Car & Truck (Business), I am pretty sure that this year has been all in the Business Category though.

In the Food & Dining, there is a category for groceries. I put 95% of my groceries under the other shopping category simply because I buy all my HBA, grocery, and General Merchandise in the same trip. The part that says Groceries is when I go to a grocery store, if we run out of something before the next shopping trip.

The Uncategorized in the month of February, was what it cost us for the repair of the busted radiator.

[table “5” not found /]Now let’s break everything down a little bit. The reason I think this is a little strewed, is because if you look at my uncategorized. I don’t have many things uncategorized, but yet the Avg. Spending for Last Six Months were I made $915? The only thing I really put in here that was uncategorized was my repair for the damage, my automobile totaled payment, and my income tax payment. But this is for spending, so I am not sure what this is actually telling me. I will have to do research.

So here is all my spending. I do see some places I can drop to make some wiggle room, but the thing is. Now that I have all this information compiled. How do I go about making a budget. Average everything together? I am decent at doing a budget for my Monthly Utilities & Credit Cards. But I really don’t know what to do with the rest…

Any suggestions?

So food and dining doesn’t include groceries? It is eating out only?

If you stop eating out you could have both of your store cards paid off by July.

You are right about this. This is something that the wife and I have talked about. We plan to cut back on this heavily, probably have to leave some money in the budget for just in case we won’t be back moments though.

And to turn the wheel around, tonight the wife and I will be eating out, for my best friend’s birthday. He rented a limo and bought tickets for us all to see Gavin Degraw. This will be the first time that the wife and I had a night out in over two years. We won’t be spending much for we are eating at home first. So we will probably just share an appetizer.

I am not sure if I will have them paid off by July, simply because it seems what everyone is suggesting I do is start an emergency fund.

And an emergency fund might be the right next step. When I looked at your budget eating out was the first thing that jumped out at me that was a “want” not a “need”. By making a 90 day sacrifice you could obliterate the rest of your Store CCs or have over (roughly) $700 in an emergency fund.

I would spend some time retagging transactions with categories that make sense with you and your spending. For me I find it very difficult to grasp the auto-classification of most programs. Prime example is groceries fall into multiple categories, as does entertainment and dining out. So in reality even though its broken down in categories you have no idea how much you are spending on groceries. Its more confusion then its worth!

I have been using mint for years. I created several of my own categories, which you can add as subcategories to a higher total.

For example: I have a $300 monthly budget for “Entertainment” under entertainment I have:

dinners (so I know how much we eat out – preventable expense)

lunches (so I know how much not planning ahead costs us)

alcohol/bars

misc expenses (coffee shops, little splurges, etc.)

tickets – for events etc.

Then you can set a budget for a large category, but still have the breakouts for individual parts if you are looking where to trim. Yes, it takes a lot of thinking about where you want categories and manually setting them up but it makes more sense to me. Also, eventually mint will start learning where you want certain transactions categorized which makes things easier.

This would also help with classifying and keeping an arm around business expense! You would be able to tag gas for your business truck separately than for your personal vehicle.

I do have these broken down into categories and subcategories. I know exactly how it is laid out, and this is what works for me. Let’s take your examples, my groceries fall into multiple categories, All my main groceries are in my Other Shopping with the exception is if during the week I have to go to the grocery store for a very hot coupon sale or if I run out of something. Most of the time I don’t run out of things, since I have a pretty big stockpile, so most of the time it is the coupon deal. The dining out and entertainment have to be broken down into two categories for tax purposes. The ones that are marked with Business have a tax deduction.

I also use Mint… and I use Quicken Home & Business.

For your big example, that can’t work for me. 9/10 times we have lunch at home, with the exception of a doctor appointment. When we eat dinner, it is usually in the same category. We keep our son to a strict schedule for the most part… While yes I could pack a lunch for all of us when we have these appointments, so you do have a point. I am cutting eating out for the most part, so this won’t be the case for much longer. Unless it is business related… I don’t need all those sub-categories for certain categories.

I love the point with budgeting into individual parts.

Additionally this will allow you to say I want to spend xxxxx on discretionary spending. Having multiple categories roll up will help you stay on track without you having to say $100 to cigarettes, $100 to fast food, $50 kids, etc.

I really don’t mean to be the first poster.

I think I figured out what you are trying to ask. It might be helpful to set up sub-savings (i use capital one 360) for items that a pretty irregular. Fund it up to a point and refill any time you dip into it. For your case, maybe auto expenses, unexpected damage..etc). And then pull from there when those things come up. I find zero-based budgeting helps me a lot and maybe it might be useful to you. Just consider savings an expense.

Out of curiousity, why did your ciggarette allowance go up in march? $67 on fast food alone seems a lot in addition to the $112 on eating out. Maybe push some of that money more towards groceries and try to cut down on some? If you regulate your meals out (twice a month or sthg) you might be able to cut it down.

I work in accounting so this might be why my mind goes here – but why do you combine your business income and expenses with your personal? From a tax point and even just an accounting point, it might be helpful to take the time to separate it. Not really budget related but maybe something to think about.

Do you give yourself an allowance? I do that and that’s where any money for fast food or things like the cinema come out of. That way, when it’s done, it’s done. Just throwing some suggestions out there.

I really don’t mean to be the grammar police and this is the last I’ll comment on it. I know you said you’ve been blogging for a while, but honestly, spelling and punctuation go a long way. Especially punctuation :). Okay that’s all i’m going to say about that.

PS. I think the word you were looking for was “skewed”.

haha, wasn’t the first.

What exactly is zero based budgeting?

Well to be honest the cigarette budget is around that every month. It is skewed as I stated, for the last three months of last year, we used our change to fund the cigarette habit. We were cutting back, (I am at 1/4 pack a day), but with my wife getting off one of her medicines it made her anxiety go up more, which turned to her smoking more.

To be honest about the business income and why I co-mingle. The reason is because I am self employed, and still a sole proprietor, I take all the money that I make for the most part except for what I save for self employment taxes and pay myself it. If there is an item I will need I do save up for it, in my business account. Later this year I am incorporating depending if my latest venture pays off. Not sure if it will be a LLC or S Corp. I do have them for the most part separate (they are in two different accounts) but I pay myself with a check for the majority.

We do not give ourselves allowances, well that’s a lie. For the most part I have been allowing my passive income this year go to trying to buy inventory and things for my wife’s direct sales business.

Haha, the way I reply is paragraph by paragraph and I realized I wrote strewed (which also could be used after I looked up what it meant) and I wrote skewed in this reply. I am pretty bad at punctuation. I have always been. Not sure how to correct this without researching more on it, and to be honest that is not a high priority. I mean come on, did you see how a past blogger used to write? Not going to mention names, but I hated reading her posts… there weren’t even paragraphs.

Nice job on tracking expenses for the last three months. Was there anything that surprised you in particular when you were doing the tallying?

A bit of advice I have discovered in the years I have been analyzing my spending is to beware of the “other” category. This category has always been easy for me to justify and can get out of hand. After a few months of tracking spending, I decide what I’m going to focus on. If my coffee shop spending has been outrageous or my shopping, then I hyper-detail track just those categories. This might mean breaking receipts down to clothing vs. food vs. snacks vs. personal care and tracking that. For me, it meant just buying food a the grocery store and banning Target except when I had a gift card, because I have ZERO self control at Target.

The other thing I like to do in tracking spending is split my categories between my routine bills and my discretionary categories. Rent/Mortgage, car insurance, utilities in one section and the groceries, entertainment, shopping, fuel and gifts into a seperate. If I were you, I would group all business expenses together as well. Be careful in how you classify something as business versus personal also.

There wasn’t anything really surprising to me when I tallied it up. But I am a little excited about, that during these three months, where I allowed anything to go basically. Just so I knew what we were doing without a budget, that they were consistently around the same amount, with the exception that I could easily point to.

Like for instance, the kid’s they were between $75-100 with the exception for March where my son just got his pictures done. And even food & dining were consistently the same except for February, where I spent $100 from our Tax Return to Eat at a Habachi Restaurant.

This is really the question I was getting at with this post how exactly should I go about doing a budget. I like how you laid this out. And as you requested, all my business expenses are grouped together… it just the report that I printed out went in alphabetical order.

I think your next step in developing your budget is to identify where you can get some reductions. Go through your fixed expenses line by line. Get new car/renters insurance quotes, haggle with your cable/internet company or drop a channel tier, and figure out if there is anything do to reduce your utilities. The interest rate on your vehicle is very high – I would keep refinancing it in the back of your mind constantly. Maybe find out what it would take to qualify for a better rate with a few different sources. Your credit score should bounce back a little bit each month, so knowing what the number needs to be to get a lower rate is key.

Then start looking at your discretionary spend. Analyze every purchase. In fact, writing down every purchase on a piece of paper might help each purchase sink in. It sounds like you already coupon, so maybe make it a policy that you’ll only eat fast food when you have a coupon to do it.

Thank you Walnut, this is the great actionable steps that I am looking for. We are pretty bare back in the utilities department… We don’t have cable so can’t shave that. I do however have the highest pack of internet through Verizon, it is only ten dollars extra for faster speed. And I really don’t know how much of a difference it makes, so maybe I will test it out and go cheaper for a month.

I would love to refinance this car, but I am not sure if our credit scores will improve. Well mine might, but the wife’s not so sure about. I will get into detail probably next week why this is the case. But I will hint at that it has something to do with my first post this week.

So….I am really confused and have to agree that it looks like your six month averages are broken. Less than a $50.00 a month average for groceries for a family of 4 with a somewhat reasonable amount of eating out? Seems unlikely. I know you said a lot of it goes in the general shopping category, but why split it, especially when you also have personal care categories? It just masks where your money really is going. I would suggest that you start out with a cash envelope system because it seems that you have no idea where your money is ACTUALLY going. Simplify things and get a handle on it, then move forward. I would suggest envelopes for

Household (aka groceries and every thing bought at grocery stores…shampoo, cleaners etc.)

Auto (a small amount set aside every paycheck for maintenance and repairs)

Entertainment and Dining (dvd’s, books, coffee shops etc.)

Kids (gifts, activities, clothing etc.)

Business expenses

Replacement fund (with kids, things break and need replaced….just a small amount set aside)

Yearly fees (auto registration, AAA membership that sort of thing)

Clothing and gifts (for the adults in the house)

Holidays (this covers activities, photos,special foods, easter baskets etc.)

Blow money I think a little bit of spending money can keep thing from becoming a lot of spending money. Something along the lines of $10 a week for each adult.

Actually the groceries is probably the only thing not broken. It’s just I label them differently. I mentioned in a comment above but they are labeled so I know how much I actually have to run out during the in between times of our trips.

I can’t go to the envelope system, I just can’t. I would be willing to move certain expenses around to other accounts, but I can’t use the envelope system. It just doesn’t work for me. One thing is certain I did not mask anything here… this is how I went about doing it. But I know where every penny in the last three months was spent.

I find this a little hard to understand. I think you have too many categories. It would make more sense to me to see your monthly budget for these, and how much you actually spent, rather than how much you spent in the last 6 months compared to now, precisely because some of your expenses are not monthly

That’s just it KLM… I am restarting everything about my debt journey. I don’t have a budget, but will be setting one up after I can understand all the numbers and what I should budget for. These are the categories I used, it probably will be broken down more after I look at it. I had 1/2 day to compile all this info since yesterday was the last day of the three months.

Jim, being a fellow smoker, have you tried going on the e cig/vape trend? I started it a month back and i have spent alot less money compared to what i was spending on cigs (i was on a pack a day!). You end up spending only $10 a month for the refills approximately, you can even strech it out to $10 every other month once you cut down on the nicotine addiction.

This sounds like a great plan… I wanted to actually quit on my son’s birthday. But my wife can’t quit, and I am afraid I wouldn’t be able to quit without her quitting as well.

Switching to e-cigarettes wouldn’t be quitting … you’d still get the nicotine! It sucks because it is an addiction, but this sounds like an excuse! (Sorry! That’s just how it sounds!)

Even vaporizing is nicotine? It might be an excuse Rachel, but I do think sharing a pack between a day or two, down from a pack each is a step in the right direction. I will not make my wife quit, for reasons I probably pointed out in another comment.

That must have come off the wrong way… Just trying to say that going to e-cigarettes might be a way of still fulfilling the nicotine addiction while reducing the costs and the health side effects.

Of course, you cannot make your wife do anything! You are separate people!

Each family has to evaluate in their life what is best for them, and this is any easy area with other positive benefits (though hard to execute). But you could try to quit or go the e-cig route, even if it might be hard or you might be afraid to fail.

That is true, and I was planning to a few days ago (the son’s birthday. But I didn’t budget anything like converting over.) Now this is not an excuse or anything, but it is easier on my pockets if I just smoke out of the same pack as my wife.

I use ecigs and have the occasional cigarette. When you are ready to make a switch, I suggest trying different ecigs because not all ecigs are created equal 🙂 I tried blu and was not impressed, I found V2 to be a great replacement. My locale has a lot of vapor specialty shops, so I may go look for more options in the future.

I know you are a couponer, so if you do decide to try out ecigs, order them online and make sure to search for coupons. There are ecig coupon sites and you can save A LOT of money this way.

Hi Jim-

I have some questions about income (well, I have lots of questions, but I will stick with one category of them):

Your income seems pretty consistent for these three months in the $1500 range, is that about what it is consistently for a longer period of time, say 12 months back, 18 months back, etc?

Also, I am surprised to see consistency in your income and a large variability in your wife’s disability income. I believe the source of that money and the reason for receiving it is a private matter that you do not need to share, but is there a monthly average over the past twelve months? It seems that if there is consistently such a wild swing in size of payment it would be difficult to depend on that as a source of income.

You may have mentioned it, but the uncategorized income payment, are those one-time payouts?

I agree that using a program such as Mint might be a good way to get a better handle on the finances then trying to create the tables.

Also, as you have several different streams of income and a deep respect for your time, do you track how much is coming from each of the different revenue sources? I think that would be something worth tracking as it would help you to determine, if you were to increase your income, in which direction you should direct your efforts.

I am all for having passive income and letting it continue to generate. However, I have two phrases that continually come to mind when I see how you seem to be working several different revenue sources for your non-passive revenue (and please forgive my cheesiness for using them):

“Jack of all trades, Master of none,” and (from my field of interest, Economics) “Do what you do best and trade for all the rest!”

And, since I have virtually written my own blog post at this point (per usual), I will leave you with this: I do think you have an interesting story to tell but Debtor is really on point about the need for grammar and punctuation. The posts read like first drafts, not final edits. I gather, since your first post was a video that maybe you prefer listening versus reading material so I will offer this suggestion, before you post have your wife (or some other adult) read your posts back to you (complete with punctuation); it may help you to better catch what has been slipping through. Alternatively, Microsoft word does offer a grammar check, although it doesn’t correct for everything. (And I agree also with Debtor that I think the word you were looking for was “skewed”).

Cheers!

-Meghan

I think the grammar police need to back down! As long as Jim is getting the message across, there is no need to quibble about this. Meghan, I saw at least thirteen errors in your reply, including punctuation omissions to wrong word usage. There is a clear distinction between then and than in writing. Debtor, cigarette is spelled with one g, not two, and all months are capitalized. May we just focus on the message? Thanks!

Jim, was the repair of the radiator really over $6,000? If so, I can believe it. A radiator pipe burst in our home this past winter, and the bill to repair just six inches of copper pipe was over $600. After that, my husband learned how to repair these himself, which came in handy when two more pipes burst.

Umm, no the portion of the expense was around $650, I believe. It would be the thing that was uncategorized, which now that I think of it, it should have been classified as home improvement most likely.

The problem with the grammar and syntax errors is the readability factor, in my opinion. Too often while reading Jim’s posts, I find myself completely confused as to what he is actually trying to say. No, it doesn’t have to be perfect. We are posting and commenting in an environment with an implied relax criteria. But, posts do need to be understandable.

Meghan,

I think my income is pretty consistent, but I will go back into my data and let you know. As for my wife’s income, her’s is consistent as well… It just that if the day she gets paid falls on a holiday or weekend it can get pushed up. And since her payout is on the 3rd of the month, there are some months that this can get pushed up into the last day of the earlier month.

The uncategorized income was my income tax and my insurance payment for my totaled car. I don’t consider either income, so that is why it is uncategorized. The $44 is my state income tax.

I do track every penny of my earnings, and I do compare where I can make more with some and during certain months I choose to ramp it up, depending on what is already going on during the month.

You are exactly right with your “cheesy” names for them. The thing is what I do best is not what is best for my family and I. I just can’t work in the restaurant business. It takes away from my family, especially my daughter. We only have her half the time, and now with school half of that half time we don’t see her. Restaurant prime times are weeknights and weekends. If I did this, I would not see her. I hope you understand.

You’ve taken a great first step – looking at your spending and where its going. Now how do you take that information and make it meaningful and actionable?

– Unlike at least one previous poster, I think you need more detailed categories to help determine exactly what you’re spending too much on.

– For now, banish all “other” categories. Break down all line items to find out where your money is really going. For instance, break out “other shopping” and “Kids other”. In the beginning of this process, you need to know as much detail as possible, then roll up some categories together as appropriate.

– Definitely keep completely separate records for your business expenses and personal expenses. Your business accounts cannot be commingled with personal expenses – this is a recipe for tax headaches (if not crises!).

Good luck and keep up the momentum! You’re starting strong.

That is exactly the question I had, what do I do now that I have this information.

The only main other category is other shopping. Which is only for our planned grocery trips. Now that I look at what I typed up, the other bills & utilities is for oil. For some reason the version I have for Quicken doesn’t have a category for heat. I might add one, but that doesn’t make any sense since my oil has been high. Looks like I have to look more in depth and maybe update this post. Grr…

As I stated in an above comment, I don’t commingle my business and personal together.

Thanks for the uplift!

There seems to be a lot of confusion because of some of these categories. You know what they all mean, but we don’t. It’s also much easier to get information out of data like this if it’s all organized in a sensible way that works for you. Get rid of the categories that don’t work for you and create ones where needed. Don’t just shove the square peg in the round hole!

My suggestion, for starters, would be to change “Grocery” to “Unplanned Grocery” and create another subcategory of “Planned Grocery” under “Food & Dining” and move everything from “Other Shopping” there. That gets all your food expenses in the same category, which is easier to handle and see what’s going on. Look for other places that don’t quite make sense and do the same, like your oil.

And yes, stop using other or misc categories. The only time I use them is if I think I don’t foresee ever having an expense like that again. Even then, I make a special note of what it was. If it pops up a couple more times, it goes into a regular category, even if I have to make a new one.

As for what to do with it, this is the starting point to a budget. Use the averages where they make sense, and make an educated guess where they don’t. Just get some numbers to start with and that don’t exceed your income. If it does, pare down where you can until it does. Then, keep tracking and try to stick with the numbers. If it just doesn’t work, adjust it for the next month until you find a budget that works. Once you have a budget that works and you’re sticking to it, where your money is going gets a lot clearer.

Also, zero based budgeting is just income – budgeted expenses = zero. Expenses include savings, and every dollar gets a job.

Perhaps a program like Mint, LearnVest or even You Need a Budget would be helpful here. Some have free trials, and perhaps they would cut you a break since you’re regularly blogging. And quit smoking! 😉 (I know, easier said than done… but really… stop!)

Thanks for the tips Angie, I will look into these and report back!

Except that it is, in that it is contributing to your financial insecurity.

Sorry..that was meant in response to your smoking not hurting the kids!

Gotcha! You are right, it is hurting us financially… I don’t really have a reply to this, as I don’t know what to say.

And I don’t want to nag you about the smoking but Pennsylvania does provide some support in helping smokers quit. Money aside it is so terrible for your health and the health of your children.

http://www.portal.state.pa.us/portal/server.pt/community/smoke_free/14315/tobacco_prevention_and_control_programs_home/557661

okay lecture over.

Thanks Theresa… It isn’t hurting our children for we only smoke outside the home, never around them. But thanks for the link, I will be looking into this.

New studies are showing that even smoking residue in your clothing and hair may be hazardous to your kids. I know that the point of this blog isn’t smoking cessation, but it’s bad for your health in addition to having bad financial implications (cost of cigarettes, exacerbation of routine illnesses, onset of chronic illnesses).

I never heard of that, but thanks for pointing it out KLM. You are right it is bad for all the reasons you have mentioned. We have been cutting back for a while now. Maybe soon we will be able to quit.

In the short term you may not be think it hurts them, but when you get lung cancer or have bad cardiovascular disease at age 50, it certainly will.

Not to be a knit picker but…..I just wanted to point out how many times you say that you/your wife can’t do something. You have stated that you can’t use the envelope system, your wife can’t stop smoking, you can’t work in the restaurant industry. Perhaps you should examine how many of these are really can nots and how many are will nots. It’s a perception thing. It is perfectly acceptable for you to be unwilling to do things, but saying that you can not do them is different. Sort of like saying you “need” a new whatzit when a used one would do.

Yes, this exactly.

I observed the same thing.

Jim, it might be helpful for you to read through your responses to suggestions and note how many time you state flat out something won’t work or is opposite to what the commenter says. (Another example is that you say your income is steady, yet the chart you provided seemed to indicate it fluctuates widely from roughly $1500 to $9000 per month.)

Take a piece of paper and write out each suggestion you contradicted and then think about why your reaction was to dismiss the suggestion with a “can’t” or an explanation. Ask yourself honestly if the explanations sound like a justification or a clarification.

Maybe your answers to yourself will give you some insight into how to change behaviour and make quicker progress on getting out of debt.

Me too! Observed the same thing.

We got through phases in this debt reduction thing .. sometimes our heads want to be out of debt, but it takes awhile for our actions to catch up (often because of unconscious barriers!)

This is what I see here.

Example: my sister wanted to reduce her expenses, but kept spending 800 dollars a month at the grocery store and lived in 1200 dollar apartment. It took her about 6 months to transition to an 800 dollar apartment and reduce her grocery trips down to 1x per week (and her grocery bill down to 400).

It can be done, but our actions have to catch up with the talk.

How exactly is my actions not catching up to my talk. We started blogging here two weeks ago, there was nothing here that was stated that I took actions. That was the reason for this post, so I can start taking some action.

Exactly! The reason for doing this blog is to take action, but it is a process! Changing behavior is a process that takes years and months, not just two weeks. So yeah, you’ve started, but there’s still a way to go.

Another example, nothing to do with your personal situation: I want to save an emergency fund (so I talk about wanting an emergency fund), but for several months I am unable to save, until I make changes in my behavior that diagnose the problem of why I was unable to save (For example, taking out savings at the beginning of a paycheck cycle, versus the end) to start to be able to save more than I previously did.

Rachel,

This is what I was hoping to do. I just have to figure out exactly how much I need every where and make that budget, to see how much I can realistically save every month

No Kate, I don’t think everyone is reading through the comments. My income is steady, I mentioned in another comment, that we make roughly $3000 every month. The numbers are a little different, the $1500 month was a month when we got my wife’s disability money early because of either a weekend or holiday. The $9000 month had the uncategorized payments which were my auto insurance payout and income taxes.

I gave almost all my explanations to why I don’t think I “can” do something. But I will re-evaluate things. Thank you.

What I don’t understand is that people think that I am not making an effort or anything. What they don’t see is in the last four years I paid off the remaining $19000 in student loan debt I had. And that I paid off another $12000 in “stupid” debt. I was on the earmark of being debt free by the end of the year if it wasn’t for the new car loan.

It is because of my behavior that I have been able to do these things. It is because of my behavior that we don’t have the luxuries that many people take for granted. Cable television & Cell Phones. And it is my behavior that decided I wanted to take my life and let it be scrutinized over strangers, so some of them can judge me and others can help me.

I know that this might come off as rude, but I am not trying to be. I honestly have been enjoying commenting back to most people, there is one that I probably didn’t. But what I wanted to get out of this post from this community, was to help me start a budget. And for the most part it was all criticism. But the thing is even through all of it, there is some gold nuggets that I got out of it.

I freely admitted, that for the last three months as an experiment I didn’t use my “behavior” and let us do things with restriction. Just so I know what the real numbers were, and I can start to adjust accordingly. And really narrow everything down, things I can work on and where the average amount was, so I didn’t cut myself short in categories that I really can’t afford to be short on.

Hope that everyone understands this.

I am not trying to come off as rude when I type this… But for one, I have tried the envelope method, it didn’t work for us. Two, my wife suffers from depression and anxiety, she is able to maintain it much of the time, due to medication. Recently, she hasn’t been taking this medicine for reasons that are personal (I probably mentioned it, because I remember commenting on it). I will not ask her to quit smoking when this is her outlet when she starts having panic attacks. But three, this you are correct on this is not I can’t work in the Restaurant Industry, I won’t. My family time is too important to me.

See…..you reexamined which things were can nots and which were will nots! 🙂 Turns out none of the three were can nots, but rather choices/ had been tried before. That was my point. You seem to be taking offense where none was meant. If we were just gushing praise, it wouldn’t be very helpful, would it?

I wasn’t taking offense to this. I wrote, then rewrote it, then rewrote it again… and every time it kinda sounded rude and I didn’t want to come off that way.

Few clarifications:

– Is your income stated after tax? If so, I think a safe estimate to base your monthly budget off of is 3,000 take home.

– What is the payment and term length on your car? Is $804 the monthly amount?

– What is the total amount paid for oil for a full winter?

– Are you medical expenses for the past 6-months normal? $50 a month to include prescriptions and visits seem low for having one person on disability. I just want you to be realistic with this number.

– Are you really spending $600 a month at general stores including groceries? Or does this amount have some christmas presents and other purposes snuck in?

I think the only difficulty you are going to have using previous numbers to make your budget is that several unexpected things have popped up along the way. They are a little difficult for us outsiders to grasp whether expenses were expected or not. Mainly the changing auto costs that seem to have skewed both maintenance, payments, and

Most people starting their debt repayment journey are really top heavy on discretionary spending. After analyzing your budget I’m finding the opposite to be true for you (my quick estimate is $375 which is pretty good). Its your needs and bills that seem disproportionate to your spending.

Additionally, who gives a crap about grammar? Its a lost art that does not have much purpose anymore as long as you are close enough to understand. Keep writing the way you want. There is nothing wrong with stream of consciousness as long as you convey your point! Its a blog not a professional journal article. Geez.

All the income stated is after Taxes Angie. And you would be totally correct, that the monthly income is or around the $3k mark.

My payments is roughly $361, for six years… The $804 is one of the skewed amounts I was talking about. Up until this month my car payments were $220, but last month I put around $4k on the down payment of the new van. As stated I don’t think the six month report I will be doing again, since it didn’t do what I thought it would do.

So far since I started putting oil in October we spent $3000.74, with perhaps another payment of around $350 this final month.

Yes the $50 a month is very reasonable amount. My children are in the CHIP program, and never had to pay really anything out of pocket. My wife’s monthly premium is automatically deducted each month before we even receive her check. With her coverage, we do not pay any co-pays… and the most I ever spent on a prescription drug is roughly $6.50. While most of them are either $1.10-$3.30.

You are right about the difficulty, that is why I came to the BAD community for some guidance. The changing auto costs aren’t that much, since this is pretty new car and I don’t expect much in this first year. I do lots of the maintenance myself, so usually just the cost of parts.

Thank you! It seems that you might have nailed it exactly about my budget. I have cut out many things in our lives that needed weeding out. Granted there are some things that def. needs improvement (i.e. my eating out) but for the most part it is the bills to my income. Well at least that is how I am reading this paragraph. Thank you for understanding!

My only comment on the cigarettes is that I think you are brave to put it out there. And I’m glad you are tracking it.

I don’t have that addiction but spend far too much on 100 cal packs of Baked Cheetos and soda. I’ve given up soda for Lent and it has been really rough (a month in I still crave it and to make matters worse weigh 3lbs more despite dropping 300 calories a day from my diet.) If I’m having a tough time with something that is only habit-forming, not physically addictive, I’m not going to judge you, just encourage you when you decide to tackle this issue.

BTW: knowing what makes you want to smoke is an important first step. Since going out for a smoke with your wife is the habit that triggers you, perhaps every second time you go out, you could grab a coffee or something else instead so you still have the break with her (a good thing), but start to cut your intake (also a good thing.) When my father-in-law quit, he identified that he’d often have a cigarette when he needed time to think through a problem at work so he gave himself permission to pause for the length of time he would have taken for the smoke. That gave him the ‘breather’ from the situation he needed to escape from, but he didn’t have to smoke. Not sure it will work for you (he had extraordinary self-will) but it might be a strategy to try.

Thanks Kate! We have been cutting smoking for over a year, but this last month my wife was having trouble with it. She noted this and does want to get down to what we were again.

Not many of the times do I personally go out to smoke with my wife. I am still down to four cigarettes a day. It’s just a little hard for me to fully quit… not saying that I won’t because she won’t. It’s just a little harder because she still smokes.

Thanks for the suggestion about the smoking!

Somewhere you said that you can’t refinance the van because of your wife’s bad credit-which won’t improve because of the mortgage situation with the ex (I assume). Does she have to be on the loan though? I know this differs from state to state but I think if you just use your income you should be able to eventually refinance. It is worth looking into. Do you have a credit union that you could become a member of? They are generally very fair lenders.

I am a member of a credit union, but I haven’t tried to quite yet. You would be correct in assuming that is the reason. That is the big reason! But I don’t won’t to spoil anything, for if I did that, I wouldn’t have anything to post about on my weekly post. She does have to be on the loan, for the debt/income ration part of the loan. I had a huge fight trying to get this loan, because they wanted to base my income solely off of Line 12 of our 1040 income and not on my 1099s and W2s.

If you know anything about taxes line 12 is about business income & losses, this is totally after all deductions and everything. These last two years I didn’t claim all my deductions, for the simple fact if I did I wouldn’t be able to claim the Earned Income Credit. I could have easily showed that my business only made a dollar, but instead I left it where I had $11,000 income and paid all my taxes on that which came to about $200, but received the max EIC on one child. If I claimed every deduction I would have been able to pay $0 in taxes, but not receive a refund.

Hope that explains a little.

Hi Jim,

While I do agree with some of the other commenters regarding grammar, I do think the comments coming back are a little harsh regarding your numbers/organization. I think the disconnect is that the majority were expecting to see a budget, not just a bunch of numbers that don’t really make sense to us since you categorize them a little differently than some (i.e., groceries going under Other Shopping rather than groceries).

What I did in setting up my budget (which granted was much simpler since I don’t deal with any home/utilities or dependents) was make a list of all categories that I might spend on in any given month. With these, I took a reasonable guess at what I should spend/save in each of those categories. For you, it should be a little easier, since you have all the raw data. I’d personally use your six month average rather than your data from the last 3 months since you said you didn’t restrict those. The important part for me was adjusting. My first few months were okay, but as I saw categories where I had money leftover, I simply made them less the next month. I also challenged myself if I was just meeting a category. For instance, my groceries (I include all household expenses in this) were 300/month. I was comfortably meeting it, so I cut it to 200 forcing me to figure out how to cut 25/wk. My quality of food/household items didn’t really diminish and all of a sudden, I had an extra 100 bucks/month. I think when you get to that step, that’s where you’ll really start to see improvement.

This is probably the exact reason. The fact of the matter those numbers weren’t my budget, and I don’t think people realize that. I wanted to experiment these first three months, to see where every cent of my money was going. I put them in categories that I could easily understand. This was not the budget… In fact it was a post or cry for help on how to start one. Thus the name of the post, Starting Jim’s Budget.

See I wanted to use that six month average, but I think some big numbers skewed things up. Like for instance my auto down payment, screwed up the car payment number. See I don’t think I could go with the average, since these last three months I didn’t restrict things, while the three months before that I did.

I really like that idea Jasmine and I appreciate you bringing it to my attention. I will be mulling over these raw numbers and see where I can improve and what every category should be. Thanks so much!

I would like to make sure I’m interpreting the business items correctly because otherwise they painted a challenging economic picture to me.

Using the 3-month totals, with a little rounding

Business Revenue: $4500

Business Expense: $3100 (auto, advertising, postage, misc, and supplies)

Business Operating Income: $1400

Let us make the assumption that you have already accounted for business taxes (payroll, unemployment, workers comp if applicable) and that your $1400 operating income for 3-months is after social security, federal and state income tax withholding that you will owe.

Unless the $2077 supplies for February was an outlier, this means you are clearing under $500 per month from your business. If you’re putting in 40h/wk on this, that’s about $3 per hour.

Even if the $2077 supplies was an outlier and lets say $100 is more normal, then your 3-month operating income is about $3400, so $1133 per month or approximately $7 per hour.

Unless you are spending less than 40h/wk, or if you see the potential to significantly grow your business revenue and income, my thought would not first turn to how to reduce your expenses to get out of debt, but rather how to increase your revenues — more work hours, a separate part-time job, or going back to work for someone else.

Can you make your business earn (after expenses and employer and employee taxes) more than $14K per year? Or should you consider a job that will allow you to earn more than $7 per hour after tax? That’s roughly $8.75/hr before tax, say $17500 per year.

Or maybe I’ve read this all wrong?

Hey AS…

I want to mention something here, my business income and gross and net are two different things. I make more than what is stated here, but it stays in the business. Which will be even more if some things I have in the works, pans out the way I hope it will.

Basically my revenue is that I, first take out for all taxes that I have to pay. If the business needs something big, I move that to my business savings account. Whatever is left over, I pay myself. This will change when the business incorporates either this year or next year.

All those expenses except for the supplies noted in February are paid out of my income. But the reality of all this, all these expenses actually help me more than they hurt me, come tax time.

If we talk about time worked, if I calculate the time into how much I would make would be a little over $26/hour. If I calculated the hours I used that pertained to generating money it would be about 14 hours per week. As I have stated I am laying a lot of pipes that does have the potential to really significantly grow my revenue. I haven’t decided if it will change the income.

As I stated I am building a lifestyle business, if I devoted more time to do parts of the business, I probably could make some more money. At the cost of time. Right now I am devoting my time to lay these pipes, where in the long run will help me out more significantly then me doing independent contractor stuff.

Hope you understand, but if I am not clearly saying well enough just keep asking and I will keep answering. 🙂

Not sure I followed all of that, but the points I took away are:

– You put in about 14h/wk

– You draw roughly $1400-1500/month as “pay” from the business (using $26/hr)

– You think your revenues will increase significantly later this year but you may keep your “pay” flat.

I didn’t follow the points on expenses helping with taxes, and whether you have to pay for supplies out of your “business revenue” or your “pay”.

I’m glad you’re earning a much better pay rate than $7/hr — $26/hr is much better – and in that case I would suggest you be totally focused on increasing the hours or revenue potential of the business. After all, if you increased your take-home pay by working more hours, and could earn an extra $200-300/month, that would go a long way towards paying off debt, and with your current time investment in your business it seems like that’s doable.

With the increase of business revenue I am hoping to generate. For the first few months of this venture, I want to reinvest all of the profits from that one venture back into the business.

As for tax breaks, right now just the mileage I put on my car, can take me down to almost zero dollars I have to pay on taxes. This is huge! Especially if you look at the percentage self employed people pay on taxes.

I do plan on being able to bring my income up, but just not right when the venture starts generating income.

Jim-

I was just looking at the tables above and I noticed that in the three months of tracking income and expenses this year that your expenses outspent your income by almost $1200, is this accurate? I am guessing the overage was caused by either the car down payment, unexpected oil expense, or the unexpected repair from running out of oil. Did you use a credit card to cover the difference?

Cheers,

Meghan

Meghan,

I am surprised you were the first one to point that out. Not saying that because it is you, but I really thought someone would point that out right away. But you would be correct, and if I took the guess as to the why, it would probably be a combination of all three of them you mentioned.

You see in December I usually make an extra $1500-$2000 through tips through my clients. Last year this extra money filled my oil tank allowing me to not have to pay oil in the month of February. This year I did fill my tank in January, and I had to for oil in February. So there was that. The rest of the money that I made from those tips, went to add to my down payment of the car. Now when my income tax came, it was supposed to get back our savings and pay off the two smaller credit cards. Well, this went to the repair from running out of oil.

I haven’t used any credit cards besides the two store credit cards in over two years. I actually paid off two other credit cards last year and closed them. The one that is being paid off this month, that gets used only seasonal if my wife needed clothes. And the other is for a big box store and that hasn’t been used in about a year.

Hope that answers your questions. Feel free to fire away.

Hey Jim!

Keep up the great work. I could care less about your grammar, really…does it even matter. My thoughts, you can’t change what you don’t acknowledge. You have acknowledged your need to get out of debt, your need to support your family and your wife. Putting your numbers out there..that’s courage. Now you can SEE. I always get confused when budgeting for items that are quarterly payments or every other month. For example my water bill is every 2 mths averaging $90. I try to make a payment every month and the month it is due, I pay the balance. That way I am usually off maybe a few dollars. For groceries, my family including my sisters and nieces coupon. It does take time however being able to spend $10 for 20 bottles of shampoo and conditioner or $20 on 40 12 packs of toilet paper is amazing. Then I don’t have to buy those items for what seems like forever. Usually free deodorant, tooth brushes, tooth paste and body wash/soap makes the time spent gathering worth it. Have you tried to roll your own smokes. My hubby and I both smoke–yes–ducking the fruit now, however we usually can roll 2 cartons of for under $20. That is really helpful.

Keep up the good work!

Connie